TL;DR

- The UL 2799 standard defines zero waste to landfill as 90%+ diversion — and seven proven technologies are making that benchmark achievable at industrial scale.

- AI-powered sorting robots now process 80 picks per minute at up to 99% accuracy, dramatically outperforming manual sorting and reducing contamination.

- Anaerobic digestion has grown to over 39,000 facilities worldwide, processing 370+ million metric tons of organic waste annually while generating renewable energy.

- Digital asset recovery platforms are projected to reach a $17.2 billion market by 2032, giving investment recovery professionals powerful new tools for surplus disposition.

- Organizations combining multiple technologies in a layered diversion hierarchy — reuse, recycle, compost, recover, then landfill — are consistently exceeding 90% diversion targets.

Why 90% Diversion Is the New Industrial Standard

Global municipal solid waste generation is on track to reach 3.4 billion metric tons by 2050 — nearly 70% more than current levels. With less than 20% of waste properly recycled worldwide, the pressure on corporations, municipalities, and investment recovery professionals to rethink waste management has never been greater.

The UL 2799 standard has established the benchmark: facilities achieving 90–94% diversion earn Silver certification, 95–99% earns Gold, and 100% diversion earns the coveted Platinum designation. Companies like Samsung Electronics — which earned Platinum across all 22 global manufacturing sites in 2024 after recycling approximately 1.32 million tonnes of waste — are proving that zero waste is not aspirational. It is operational.

Landfill diversion rate required for UL 2799 Zero Waste to Landfill certification

What is making these numbers possible? Seven technologies — each addressing a different segment of the waste stream — are converging to create integrated diversion systems that consistently surpass the 90% threshold. For sustainability and asset management professionals, understanding these technologies is not optional — it is essential for staying competitive and compliant.

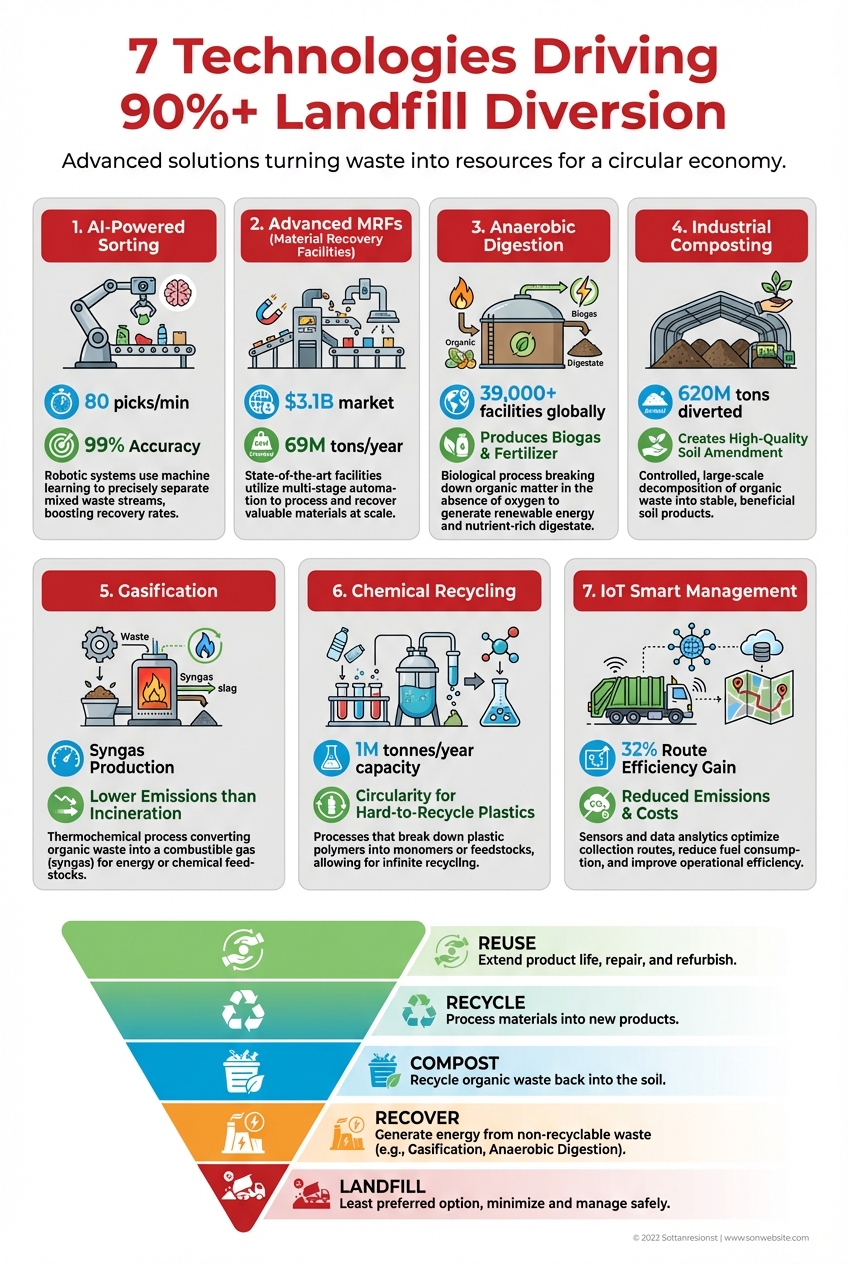

1. AI-Powered Sorting Systems

Artificial intelligence has fundamentally transformed material recovery. Modern AI sorting robots use optical sensors, near-infrared spectroscopy, and deep learning algorithms to identify and separate materials at speeds and accuracies that human sorters simply cannot match.

AMP Robotics, one of the technology leaders, reports that its AI-powered robots sort 80 items per minute compared to 35 by a human worker — with accuracy rates exceeding 95%. ZenRobotics, now owned by Terex, has developed systems achieving sorting accuracies of up to 98% for construction and demolition waste. In November 2024, TOMRA Recycling introduced its next-generation AUTOSORT system with deep learning AI, achieving 99.5% accuracy in sorting mixed plastics while reducing contamination by up to 60%.

Investment Recovery Connection: AI sorting is not limited to municipal waste. The same technology powers asset recycling and disposition optimization, helping IR professionals identify recoverable materials in mixed surplus streams with unprecedented precision.

The robotic waste sorting market stood at $2.84 billion in 2025 and is projected to reach $6.66 billion by 2030, reflecting an 18.59% CAGR. North America alone hosts over 400 AMP Robotics units, and Waste Management invested $1.4 billion in AI-enabled facilities between 2024 and early 2025. As AI capabilities continue to accelerate, expect sorting accuracy to approach near-perfect levels across all material categories.

2. Advanced Material Recovery Facilities (MRFs)

Material Recovery Facilities are the backbone of modern recycling infrastructure, and the latest generation of MRFs bears little resemblance to the facilities of even a decade ago. The global MRF market reached approximately $3.1 billion in 2024, with North America’s 300+ facilities collectively processing more than 69 million short tons of recyclables annually.

What distinguishes advanced MRFs is their integration of multiple sorting technologies: optical sorters, eddy current separators, ballistic separators, and increasingly, AI-powered robotic arms. Large-scale MRFs equipped with this technology stack achieve dramatically better economics — consuming just 5–90 kWh per metric ton of recyclables compared to 300–550 kWh for smaller facilities, while capturing significantly more value from plastics (33% of revenue versus 5% for small MRFs).

AMP Robotics recently launched its first fully integrated AI facility designed to process 62,000 tons per year of single-stream recycling. These secondary sortation facilities aggregate difficult-to-recycle mixed plastics, paper, and metals from primary MRF residue — recovering materials that would otherwise go to landfill and representing a major opportunity to boost national recycling rates. For organizations pursuing circular economy asset management, advanced MRFs are critical downstream partners.

3. Anaerobic Digestion

Anaerobic digestion (AD) has emerged as one of the most scalable and economically viable solutions for organic waste diversion. By breaking down food waste, agricultural residues, and other organic materials in oxygen-free environments, AD facilities produce biogas for energy generation and nutrient-rich digestate for agricultural use — diverting organics completely from landfills while generating revenue from two product streams.

Anaerobic digestion facilities operating globally in 2024, processing 370+ million metric tons of organic waste

The numbers tell a compelling growth story. The global AD market is projected to grow from $65.48 billion in 2025 to $105.69 billion by 2032. In the U.S. alone, more than 2,300 operational digesters are now active, including over 400 on livestock farms and nearly 70 dedicated food waste processing plants. Germany leads globally with over 9,500 units, and European countries injected over 27 billion cubic meters of biomethane into national gas grids in 2024.

For investment recovery professionals, AD represents both a diversion pathway for organic waste generated in industrial operations and a growing market for equipment liquidation as facilities scale up and upgrade their processing capacity.

4. Industrial Composting at Scale

Industrial composting complements anaerobic digestion by handling organic waste streams that may not be suitable for AD — including yard waste, certain food-soiled paper products, and agricultural byproducts. Global organic waste diversion through composting reached more than 620 million tons in 2024, with over 120,000 composting facilities operating worldwide across residential, commercial, and agricultural sectors.

The growth trajectory is steep. Municipal composting programs increased by 24% between 2023 and 2025. In the U.S., composting facilities processed over 14.3 million tons of organic feedstock in 2023, producing approximately 6 million tons of finished compost — up from 5.2 million tons in 2021. The global food waste composting machine market alone is projected to grow from $12.4 billion in 2025 to $28.4 billion by 2034.

Sustainability Impact: California’s SB 1383 mandates a 75% reduction in organic waste disposal by 2025, requiring 75–100 new large-scale composting facilities statewide. This legislation is driving a national shift toward mandatory organics diversion — creating both compliance obligations and sustainability success opportunities for forward-thinking organizations.

5. Gasification and Advanced Thermal Processing

Gasification converts non-recyclable waste into synthetic gas (syngas) through partial oxidation at high temperatures — offering a cleaner alternative to traditional incineration with lower emissions and higher energy efficiency. A comparative evaluation of over 350 peer-reviewed papers found that gasification is superior to incineration and pyrolysis in terms of harmful emissions and energy recovery.

Innovative developments in catalytic gasification and plasma-assisted gasification are pushing the technology further. These advanced methods convert municipal solid waste into high-quality syngas with improved efficiency, reduced tar formation, and increased yields. For facilities handling mixed waste streams that cannot be mechanically recycled or composted, gasification provides a critical diversion pathway that keeps materials out of landfills while recovering energy value.

The regulatory environment is accelerating adoption. India’s April 2024 amendment to its Solid Waste Management Rules bars mixed-waste landfilling in cities above 100,000 population by January 2026. Circular economy agendas across Europe, Asia, and North America are driving utilities to replace aging incinerators with high-efficiency gasification plants that can monetize metals, heat, and biofuels. Understanding these trends is essential for professionals managing asset disposition strategies in the energy and industrial sectors.

6. Chemical and Advanced Recycling

Chemical recycling employs depolymerization and pyrolysis to break down heterogeneous polymers into recoverable monomers, enabling indefinite recycling loops for materials like polyethylene (PE), polypropylene (PP), and polyester (PET). While the technology has faced headwinds — including plant closures by Ioniqa and Brightmark in early 2025 — global installed capacity ended 2024 just shy of 1 million tonnes per year.

The success stories are notable. Eastman completed a 110,000-tonne-per-year PET solvolysis plant, demonstrating commercial viability at meaningful scale. Life-cycle assessments indicate that chemical recycling can reduce environmental footprints by approximately 45% compared to conventional disposal. Advanced enzymatic and catalytic hydrocracking technologies exhibit conversion efficiencies of 85–95%.

Legislative support is expanding: 24 U.S. states have passed laws defining chemical recycling as manufacturing. A coalition of major brands has called for access to 800,000 metric tons of chemically recycled plastics by 2030. For investment recovery professionals working with plastic waste streams, chemical recycling opens pathways for materials that were previously unrecoverable through mechanical means.

7. IoT-Enabled Smart Waste Management

The Internet of Things is providing the data infrastructure that makes all other diversion technologies more effective. IoT sensors embedded in waste bins monitor fill levels in real time, GPS-equipped collection vehicles optimize routes dynamically, and machine learning algorithms predict waste generation patterns to prevent overflow and reduce unnecessary pickups.

The results are quantifiable. Pilot programs have demonstrated 32% improvements in route efficiency, 29% decreases in fuel consumption and emissions, and 33% increases in waste processing throughput. Barcelona’s deployment of over 18,000 IoT sensors saves the city approximately €555,000 annually in waste management costs. Deep learning-based waste classification systems using models like VGG-19 have achieved 99.7% accuracy in training environments.

For organizations pursuing zero waste certifications, IoT provides the granular tracking and reporting capabilities needed to document diversion rates with the precision that UL 2799 auditors require. Combined with tech-driven surplus asset recovery strategies, IoT-enabled waste management creates a data-rich foundation for continuous improvement.

The Layered Approach: How Leading Organizations Exceed 90%

No single technology achieves 90% diversion alone. The organizations consistently exceeding this threshold deploy a deliberate hierarchy: reuse first, then recycle, compost, recover energy, and landfill only as a last resort.

| Technology | Target Waste Stream | Typical Diversion Impact | Maturity Level |

|---|---|---|---|

| AI-Powered Sorting | Mixed recyclables | 15–25% additional recovery | Commercial scale |

| Advanced MRFs | Single-stream recycling | 30–50% of total waste | Mature |

| Anaerobic Digestion | Food & organic waste | 20–35% of total waste | Mature |

| Industrial Composting | Yard & agricultural waste | 10–20% of total waste | Mature |

| Gasification | Non-recyclable residuals | 5–15% of total waste | Scaling |

| Chemical Recycling | Mixed/contaminated plastics | 5–10% of total waste | Early commercial |

| IoT Smart Management | All streams (optimization) | 5–15% efficiency gains | Commercial scale |

Samsung’s Platinum-certified facilities exemplify this integrated model. Amazon’s diversion rate climbed from 82% in 2022 to 85% in 2024 through systematic technology deployment, including partnerships with AI-enabled sorting company Glacier. Target achieved 87% diversion in 2024 with plans to reach zero waste by 2030. AT&T has reported 98% diversion rates through organized asset recovery programs — demonstrating the direct connection between investment recovery and zero waste outcomes.

A Practical Roadmap for Investment Recovery Professionals

Achieving 90%+ diversion requires strategy, not just technology. Here is a practical framework that investment recovery professionals can implement:

Step 1: Conduct a Comprehensive Waste Audit. Before investing in any technology, quantify your current waste streams by material type, volume, and disposal method. Identify the largest contributors to your landfill tonnage — these represent your highest-impact diversion opportunities. Use IoT monitoring to establish baseline metrics.

Step 2: Prioritize the Waste Hierarchy. Apply the hierarchy rigorously: reuse and resale first (through asset recovery services and surplus marketplaces), mechanical recycling second, organic processing third, energy recovery fourth, and landfill only as a last resort.

Step 3: Build Technology Partnerships. No organization needs to own every technology. Partner with advanced MRFs for recyclable processing, AD facilities for organics, and gasification providers for residuals. The digital circular economy market — projected to reach $17.2 billion by 2032 — offers growing platform options for matching surplus assets with buyers.

Step 4: Track, Report, and Certify. Implement IoT-based tracking across all waste streams. Document diversion rates with the granularity required for UL 2799 certification. Pursue formal validation — the certification itself becomes a competitive advantage for ESG reporting and customer confidence.

Step 5: Leverage Professional Networks. The Investment Recovery Association provides the industry knowledge, ESG-compliant frameworks, and peer connections needed to benchmark your program against best practices. CMIR-certified professionals bring the expertise to design and execute diversion strategies that deliver both financial returns and environmental outcomes.

The Bottom Line: Investment recovery returns $20+ for every $1 invested — and when combined with zero waste technologies, IR professionals become sustainability heroes in their organizations. The seven technologies outlined here are not future concepts. They are commercially available, proven at scale, and delivering measurable results today.

Seven technologies driving 90%+ landfill diversion — from AI sorting to digital asset recovery platforms.