TL;DR

- EV battery recycling is a 2026 inflection point for investment recovery teams. The lithium-ion battery recycling market climbs to roughly $6.9 billion in 2026 and is projected to reach $37.5 billion by 2035, while second-life capacity scales from about 25-30 GWh in 2025 toward 330-350 GWh by 2030.

- Modern hydrometallurgical recycling recovers 95% of lithium and cobalt and 97% of nickel, turning what used to be hazardous waste into a measurable revenue line.

- Three EOL pathways now compete for every battery: refurbishment and resale, second-life energy storage, and material recycling. The right choice depends on remaining capacity, chemistry, and the buyer market.

- Regulation is converging fast. The EU Battery Passport hits February 18, 2027, and the U.S. clean-vehicle critical minerals threshold is 70% in 2026 with FEOC restrictions live. IR teams who act now have a year to build the data backbone.

- Most IR programs already own these assets: EV fleet packs, stationary BESS, lithium-ion forklifts, UPS strings, and telecom cells. Treating them as one battery portfolio unlocks scale on every RFP.

EV Battery Recycling Hits an Inflection Point in 2026

For most of the last decade, ev battery recycling sat quietly inside ESG slide decks and university research papers. In 2026 it landed on the desk of every corporate asset manager. The same is true of every adjacent category: ev battery solutions providers are scaling fast, battery management system data is being treated as core IR documentation, and the recovery channels for industrial battery disposal are professionalizing. The lithium-ion battery recycling market is projected to grow from about $6.9 billion in 2026 to $37.5 billion by 2035 at a 20.6% compound rate, while second-life applications add another curve on top of that line. Capacity is following the money: industry analysts now expect second-life EV battery capacity to scale from roughly 25-30 GWh in 2025 to 330-350 GWh by 2030, a CAGR near 65%.

The numbers matter, but the operational reality matters more. The first wave of high-volume EV fleet retirements is hitting commercial operators in 2026. Stationary battery energy storage systems built between 2010 and 2014 are starting to roll off their service life. Distribution centers that converted to lithium-ion forklifts five years ago are now planning their first end-of-life cycle. For investment recovery and asset management teams, batteries are no longer a future problem. They are the next category to professionalize, the same way IT asset disposition matured a decade ago.

Projected lithium-ion battery recycling market growth, 2026 to 2035 (20.6% CAGR)

Why Investment Recovery Teams Now Own the Battery Conversation

Battery end-of-life used to belong to facilities, EHS, or the local fleet manager. That ownership model breaks at scale. When a Fortune 500 operator has hundreds of EV vans, several megawatts of stationary storage, and thousands of lithium-ion forklift packs across dozens of sites, the only function with the contracting muscle, vendor management discipline, and audit trail capability to handle it cleanly is investment recovery.

Three pressures are pushing batteries into the IR portfolio. First, regulation is mandatory rather than aspirational. Second, the recovered material has a real price tag, which means a contract drafted poorly leaves money on the table. Third, sustainability reporting now demands defensible chain-of-custody data on retired energy assets, and IR teams already produce that paperwork for every other surplus category.

The Investment Recovery Association has long argued that IR professionals are the sustainability heroes of the modern enterprise. Batteries make that argument quantifiable. A single end-of-life pathway decision, refurbish vs. second life vs. recycle, can swing the value of a battery pack by a factor of three or four. That is exactly the kind of decision IR teams are built to make.

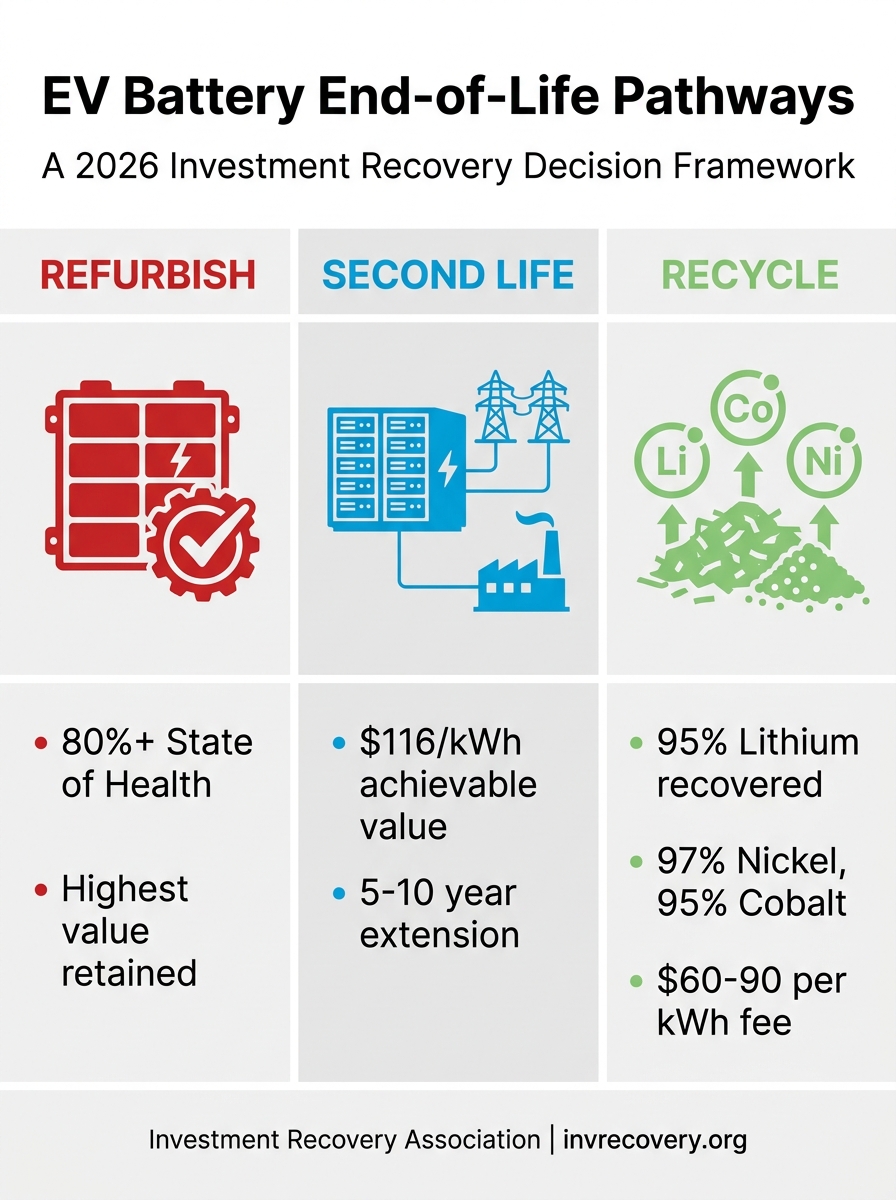

The Three End-of-Life Pathways: Reuse, Second Life, and Recycle

Every retired battery faces the same fork in the road. Choosing the right path is the central act of ev battery recycling strategy.

Reuse and refurbishment

If a pack still holds 80% or more of its rated capacity and the buyer market exists, refurbishment is almost always the highest-value path. Cells get tested, weak modules get swapped, and the pack returns to a primary application, sometimes the same one. This is the same logic the IR community has applied to surplus asset disposition for years: extract the highest use before harvesting raw value.

Second-life energy storage

Below about 80% state-of-health, automotive use becomes marginal but stationary applications remain attractive. Repurposed packs land in EV charging stations, telecom backup, microgrid storage, and commercial behind-the-meter peak shaving. Studies put the achievable second-life value at around $116 per kWh for an LFP pack acquired at 80% remaining capacity and operated until 50%. NPV analyses generally turn positive in commercial and industrial applications, even when residential numbers stay marginal.

Sustainability win: Second-life deployment can extend total battery service life by an additional 5 to 10 years, displacing manufacturing emissions equivalent to building entirely new storage from scratch. It is the textbook circular economy move at industrial scale.

Material recycling

When a pack falls below useful capacity or has structural damage, the value sits in the metals. Hydrometallurgical processing now achieves recovery rates of 95% for lithium, 95% for cobalt, and 97% for nickel, with hydrometallurgy holding roughly 70% of global recycling capacity. The recovered metals re-enter battery production at the cathode level. The total recycling fee for high-power batteries currently runs $10-15 per kg, or roughly $60-90 per kWh, before deducting the recovered-metal credit.

The three end-of-life pathways for EV and industrial batteries, with the financial and environmental signals that should guide each decision.

Asset Categories Most IR Programs Will Touch in 2026

Most investment recovery teams underestimate how broad the battery footprint already is. A single enterprise will typically retire batteries from at least four distinct asset classes. The mistake is treating them as separate problems. Pooling them into one battery portfolio unlocks scale on RFPs, simplifies audit trails, and turns small-volume categories into negotiating leverage.

EV fleet packs

Light-duty vans, sedans, and yard tractors retired between 2024 and 2026 are the most visible category. Pack chemistries vary widely (NMC, LFP, NCA), and chemistry drives recovery economics. NMC and NCA packs carry a higher per-kWh metal value because of cobalt and nickel content. LFP packs have lower metal value but higher second-life potential because of their cycle life and thermal stability.

Stationary battery energy storage system (BESS)

Utility and commercial BESS units installed in the early 2010s are now hitting their 10-15 year service life. Decommissioning typically begins within 12 months of operational shutdown and runs 6-9 months end to end. The cost stack covers labor, equipment, transport, and recycling or disposal, and it can be a meaningful capex line if it has not been planned for. The same scrutiny that data center decommissioning teaches applies here: plan the retirement contract before construction is even finished.

Lithium-ion forklift batteries

The warehouse and distribution sector converted aggressively to lithium-ion between 2018 and 2022. Five to seven year service lives mean these packs are now retiring in volume. Lithium-ion forklift batteries are denser and less hazardous than the lead-acid units they replaced, but the recycling supply chain is still maturing, so contract terms matter more than usual.

Lead-acid legacy assets

Lead acid is not glamorous, but it is the gold standard of recycling: roughly 99% of lead acid batteries get recycled in North America, and the market for the recovered lead is mature. For most IR teams, lead acid battery recycling continues to operate on standard scrap-metal economics. The play here is not technology, it is volume aggregation, the same way IR teams handle the scrap metal market. Many vendors now bundle lead acid battery recycling with lithium-ion intake on the same RFP, which simplifies logistics and tightens reporting.

| Asset class | Typical EOL trigger | Best-fit pathway | 2026 supply outlook |

|---|---|---|---|

| EV fleet packs | Lease return / capacity fade | Refurbish > second life > recycle | Volume rising sharply |

| Stationary BESS | Service life / repowering | Recycle (most common in 2026) | First retirement wave |

| Lithium-ion forklifts | Cycle life / shift fit | Refurbish or second life | Maturing infrastructure |

| Lead-acid legacy | Standard replacement | Recycle (mature) | ~99% recycled in NA |

Ev Battery Recycling Economics: Where the Investment Recovery Numbers Actually Land

The honest answer is that ev battery recycling economics are still uneven and depend heavily on chemistry, condition, and contract structure. Three numbers anchor most modern deals.

First, recovered-metal credits. With hydrometallurgical recovery rates north of 95%, a tonne of NMC black mass currently generates revenue across lithium carbonate, cobalt sulfate, and nickel sulfate that often clears the processing fee with margin to spare. LFP black mass is leaner because there is no cobalt or nickel to harvest. That is why LFP pack disposition decisions usually favor second-life pathways longer than NMC decisions do.

Second, second-life pack value. Recent academic work pegs the achievable value at roughly $116 per kWh for a pack purchased at 80% capacity and retired at 50%, with margins concentrated in commercial and industrial deployments. Residential second-life economics remain marginal because new battery prices have fallen so far, with industry forecasters expecting cell-level pricing below $100 per kWh in 2026.

Third, total decommissioning load. For a stationary BESS, the all-in retirement cost (logistics, recycling fee, site restoration) lands around $60-90 per kWh. That is a real number to budget against the recoverable-material credit and the avoided cost of new capex if a second-life pack handles a non-critical duty cycle.

IR rule of thumb: Until your battery vendor will model the recovered-metal credit on a chemistry-specific basis and expose it in the contract, you are still paying retail. The single biggest economic lever in ev battery recycling is moving from a flat per-kg recycling fee to a recovered-value share.

Regulatory Pressure: Battery Passport, CRMA, and the New Compliance Map

Three regulatory streams now shape every IR battery decision, and they reinforce each other.

EU Battery Passport. Beginning February 18, 2027, all EV and industrial batteries above 2 kWh placed on the EU market must carry a digital battery passport accessible via QR code. The first version requires basic identification, type, model, and electrochemical performance data, with due diligence obligations now scheduled for August 18, 2027 after a postponement from 2025. U.S. companies that ship products containing batteries to Europe are pulled into scope, and the data backbone takes serious lead time to build, especially for organizations with complex supply chains or low product-data maturity.

U.S. clean-vehicle critical minerals threshold. The IRA’s 30D credit requires that 70% of the value of critical minerals in a clean-vehicle battery be extracted, processed, or recycled in the U.S. or a free-trade-agreement partner in 2026. The percentage steps up annually, and Foreign Entity of Concern (FEOC) restrictions block batteries with components from FEOC suppliers from credit eligibility. Recycled content counts toward the threshold, which materially increases the value of recovered domestic material.

R2v3 and e-Stewards alignment. The same certifications that govern ITAD are evolving to cover battery handling. Vendors without one of the recognized certifications should be approached with caution: the audit trail risk is real, and the chain-of-custody documentation is exactly what sustainability and finance teams will demand for ESG reporting.

How to Select a Battery Recycling Vendor: An RFP Framework

Most IR teams already run rigorous RFPs for ITAD, surplus equipment auctions, and scrap. Battery RFPs follow the same architecture but add chemistry-specific clauses. The framework below covers the core sections.

Certifications and compliance. R2v3 or e-Stewards (or local equivalent), ISO 14001 environmental management, ISO 9001 quality, ISO 27001 if data-bearing systems are involved, and any state-level battery handler permits. Verify expiration dates rather than logos. This mirrors the discipline IR teams developed during the early years of sustainable surplus asset management.

Pathway transparency. Ask the vendor to disclose, by chemistry and pack condition, what percentage of received batteries are refurbished, second-lifed, recycled, or landfilled. Many vendors quietly default to recycling because it is operationally simpler, even when refurbishment would yield more value to the customer.

Recovered-value share. Demand a structure that exposes the recovered-metal credit. A flat per-kg or per-kWh fee is fine for low-volume programs, but high-volume IR operators should be on a tiered model with chemistry-specific revenue share.

Data and reporting. Itemized chain-of-custody, downstream auditing rights, ESG-grade carbon impact reporting, and the data fields needed for an EU Battery Passport entry. Vendors who cannot produce passport-ready data in 2026 will be a liability in 2027.

Logistics and safety. DOT-compliant transport, damaged-cell handling protocols, fire suppression at the receiving facility, and clear escalation procedures. Lithium-ion fires are rare but expensive, and indemnification language is the single clause that most IR teams under-spec.

Geographic fit. With the IRA’s domestic-content rules, North American processing is now economically as well as logistically preferable. Verify that the vendor’s hydrometallurgical or pyrometallurgical processing actually happens where they say it does.

A Six-Step Battery Investment Recovery Roadmap

For organizations starting from a standing start, the practical sequence is straightforward.

Step 1: Inventory. Pull every battery-bearing asset class into a single registry. EV fleet packs, BESS, forklifts, UPS strings, telecom backup, scientific equipment, and yard equipment. Capture chemistry, kWh, install date, and expected EOL year.

Step 2: Forecast retirement volume. Three-year and five-year retirement curves by asset class. Without this, RFPs default to spot pricing and you lose the volume premium.

Step 3: Define decision rules. Capacity thresholds and chemistry rules that determine the default pathway. For example: “NMC packs at 70%+ SOH go to refurbishment first; LFP packs at 60%+ SOH go to second-life evaluation; everything below those thresholds goes to recycling.”

Step 4: Run the RFP. Use the framework above. Negotiate recovered-value share, chain-of-custody data, and EU Battery Passport readiness as standard contract terms.

Step 5: Build the audit trail. Every retired battery gets a record: serial, chemistry, kWh, ship date, vendor, pathway, recovered material, recovered value, certificate of disposition. This is the same data discipline that makes CMIR-certified IR programs auditable in any other category.

Step 6: Report up. Sustainability, finance, and risk all want different cuts of the same data. Build the reporting templates once and feed them quarterly. Battery investment recovery is a story that boards now want to hear.

A well-run IR program returns more than $20 for every $1 invested. Adding batteries to the portfolio extends that ratio without adding a separate function.

Frequently Asked Questions

Sources and References

- Global Market Insights, “Lithium-Ion Battery Recycling Market Size, Growth Trends 2035,” 2026 – market sizing for the lithium-ion battery recycling sector. Source

- Roots Analysis / MarketsandMarkets, “Second Life EV Battery Market,” 2026 – second-life capacity and market growth forecasts. Source

- European Commission, EU Batteries Regulation 2023/1542 and Regulation (EU) 2025/1561 – Battery Passport effective date and due diligence postponement. Source

- U.S. Department of the Treasury, “Proposed Guidance on the New Clean Vehicle Credit,” 2024 – 2026 critical minerals thresholds and FEOC restrictions. Source

- Royal Society of Chemistry, “Hydrometallurgical recycling technologies for NMC Li-ion battery cathodes,” RSC Sustainability 2023 – hydrometallurgical recovery rates for lithium, cobalt, and nickel. Source

- ScienceDirect, “Cost, energy, and carbon footprint benefits of second-life electric vehicle battery use,” 2023 – $116/kWh second-life value benchmark. Source

- Renewable Energy World, “Battery energy storage system decommissioning and end-of-life planning,” 2025 – BESS decommissioning cost stack and timeline. Source

- RMI, “Understanding How EV Battery Recycling Can Address Future Mineral Supply Gaps,” 2024 – critical mineral supply analysis. Source

- U.S. Department of Energy, Alternative Fuels Data Center, “Batteries for Electric Vehicles” – direct recycling and recovery process overview. Source

This article is published by the Investment Recovery Association (IRA) for educational and informational purposes only. It does not constitute legal, financial, or professional advice. Market data, statistics, and projections cited are sourced from third-party reports and are subject to change. Readers should consult qualified professionals before making business decisions based on the information presented. The IRA makes no warranties regarding the accuracy or completeness of third-party data referenced herein.