TL;DR

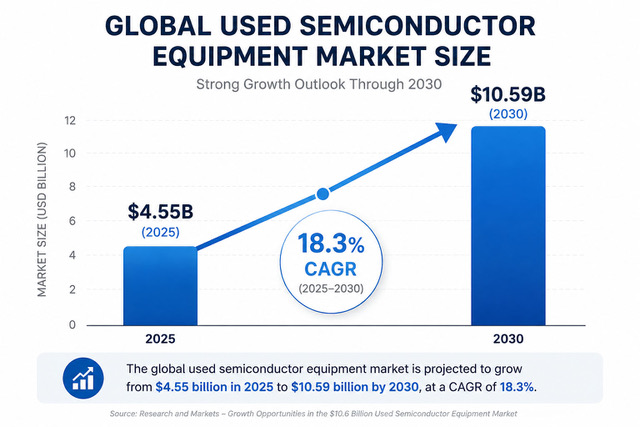

- The market for used semiconductor equipment is on track to more than double, from roughly $4.55 billion in 2025 to about $10.59 billion by 2030, an 18.3% compound annual growth rate.

- Fab refresh cycles, the CHIPS-driven build-out, and surging AI chip demand are flooding the secondary market with surplus tools, and much of it still carries six- and seven-figure resale value.

- A single restructuring can put enormous value at risk: Intel recorded roughly $800 million in impairment and accelerated depreciation on excess tools in 2025, a reminder that disposition planning belongs in the boardroom.

- Reusing a tool instead of building new avoids the carbon-intensive manufacture of a replacement, turning investment recovery into a measurable Scope 3 win alongside the financial return.

- A disciplined recovery playbook, planned before a line goes dark, is what separates full value capture from a fire sale.

When a wafer fab shuts down a line, retools to a new node, or cancels an expansion, the equipment left behind is among the most valuable surplus any organization will ever handle. A single deposition or lithography tool can be worth more than an entire warehouse of conventional surplus. That is exactly why used semiconductor equipment has become the fastest-growing asset class in the investment recovery world, and why disposition strategy now deserves the same rigor a fab applies to procurement. This playbook walks through how recovery professionals value, route, and monetize surplus fab tools in 2026 while turning reuse into a sustainability story leadership actually wants to tell.

The opportunity is real, and so is the risk of leaving money on the table. The marketplaces that dominate search results will happily list your assets, but they do not build the internal process that protects value from the moment a tool is flagged for retirement. For a broader grounding in the discipline, our guide on what investment recovery is and how it works in 2026 sets the foundation this article builds on.

Why Used Semiconductor Equipment Is the Fastest-Growing Surplus Asset Class in 2026

Semiconductor manufacturing runs on a relentless upgrade cycle. As leading-edge fabs push to ever-smaller nodes, perfectly functional tools become surplus to the front end yet remain in heavy demand for mature-node, analog, power, and specialty production. That mismatch between what advanced fabs retire and what the rest of the industry still needs is the engine behind a booming secondary market.

The secondary market by the numbers

Analysts project the global market for used and refurbished fab tools will expand from roughly $4.55 billion in 2025 to about $10.59 billion by 2030, a compound annual growth rate of 18.3%. A parallel forecast for semiconductor equipment trading puts that broader marketplace at $10.86 billion in 2025, rising to $17.75 billion by 2032. Whichever lens you use, the direction is unmistakable: surplus fab equipment is becoming a deep, liquid, and global market.

Global used semiconductor equipment market size: $4.55B in 2025 growing to $10.59B by 2030 at an 18.3% CAGR. Source: Research and Markets via GlobeNewswire.

What is driving the surge: CHIPS build-out, tool refresh, and AI demand

Three forces are converging at once. First, the CHIPS-driven build-out across North America and Asia is creating new capacity while simultaneously accelerating the retirement of older lines as manufacturers consolidate and modernize. Second, the AI boom is pulling demand toward leading-edge logic and high-bandwidth memory, which speeds up tool refresh at the most advanced fabs. Third, the same AI infrastructure wave reshaping data center decommissioning in 2026 is increasing total demand for chips, which keeps mature-node fabs, and the used tools that equip them, busy.

Key distinction: Surplus to a leading-edge fab is rarely scrap. A tool retired from a 7-nanometer line can be the centerpiece of a profitable mature-node, MEMS, or compound-semiconductor operation. Treating fab surplus as waste destroys value that the market is actively willing to pay for.

Where investment recovery fits in the fab lifecycle

Investment recovery is the discipline of extracting maximum value from idle, surplus, and end-of-life assets, and few asset types reward that discipline like fab tools. The financial stakes were underscored in 2025 when Intel recorded approximately $800 million in non-cash impairment and accelerated depreciation tied to excess manufacturing tools described as having no identified reuse. Whether those assets ultimately flowed to brokers, were refurbished and redeployed, or entered recycling streams was never publicly detailed. That uncertainty is the cautionary tale: without a recovery plan, even sophisticated manufacturers can write down enormous value rather than recapture it. Investment recovery professionals exist precisely to make sure the answer is recapture.

The Anatomy of a Fab Decommissioning: Knowing What You Have

You cannot recover value from assets you have not properly inventoried. A fab decommissioning produces a remarkably diverse asset pool, and each category demands a different disposition path. Mapping the full inventory early is the single highest-leverage step in the entire process.

Front-end process tools: lithography, etch, and deposition

The headline assets are the front-end process tools: lithography scanners and steppers, plasma and wet etch systems, chemical and physical vapor deposition chambers, ion implanters, chemical mechanical planarization tools, and metrology and inspection systems. These are the high-value items, frequently carrying resale prices from the high five figures into the millions depending on node and condition. They also require the most careful handling, documentation, and de-installation, which is why they should anchor your valuation effort.

Subfab and facilities systems: gas, chemical, and abatement

Below and behind the cleanroom sits a second tier of value that is easy to overlook: gas delivery and bulk gas systems, chemical handling and distribution infrastructure, vacuum pumps, chillers, abatement systems, and cleanroom HVAC. Some of this equipment has strong secondary demand, while some has primarily a recycling or responsible-disposal pathway because of contamination or code requirements. The principles for capturing value here mirror those in any industrial setting, and our guide on maximizing returns from end-of-life equipment applies directly.

Spares, parts, and consumables that hold hidden value

The least glamorous category is often where margin hides. Spare parts inventories, replacement chambers, robotics, electronic modules, and even consumable kits can command strong prices on parts marketplaces, especially for legacy tools no longer supported by their original makers. A tool that is uneconomical to relocate whole may be worth far more parted out. Detailed inventory photography and accurate cataloging turn this long tail into real recovery, a theme explored in our piece on maximizing ROI when liquidating industrial assets.

Valuing Used Semiconductor Equipment: What Drives Resale Price

Valuation is where investment recovery earns its keep. Used semiconductor equipment does not have a simple blue-book price; value swings widely based on a handful of factors, and understanding them is the difference between negotiating from strength and accepting the first offer.

Technology node and tool generation

The most important driver is the node and generation a tool supports. Demand concentrates around mature and specialty nodes where used equipment is the practical way to add capacity. A tool that aligns with active mature-node production holds value strongly, while equipment tied to a node with shrinking demand depreciates faster. Reading where industry demand is heading is essential, and our overview of 2026 investment recovery trends provides useful market context for those judgments.

Condition, documentation, and provenance

Buyers of high-value capital equipment pay for confidence. Complete maintenance logs, run-hour records, original manuals and software, calibration history, and a clear ownership trail all raise realized price and shorten the sales cycle. Tools that were running and supported until the day the line stopped command a premium over assets that sat idle and undocumented for years. The same valuation discipline that governs all surplus, detailed in our review of surplus asset valuation approaches, applies with extra force here because the dollar amounts are so large.

Decontamination, de-installation, and logistics costs

Net recovery, not gross price, is what matters. Semiconductor tools may require decontamination certification, specialized riggers, vibration-controlled transport, and cleanroom-grade reinstallation. These costs can be substantial and must be modeled into any disposition decision. A realistic net-value model prevents the unpleasant surprise of a high headline price erased by removal expenses, and it tells you when redeployment or parts harvesting beats a whole-tool sale.

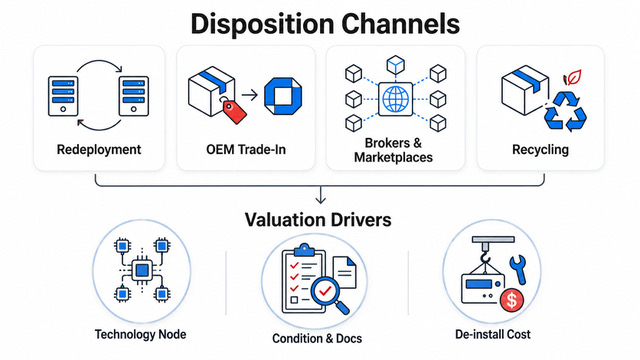

Disposition Channels: How to Recover Maximum Value

Once you know what you have and what it is worth, the question becomes how to sell it. There is no single best channel; the highest total recovery usually comes from matching each asset to the right route. The dominant search results for used semiconductor equipment are marketplaces, but a marketplace listing is a tactic, not a strategy.

OEM certified pre-owned and trade-in programs

Original equipment makers including ASML, KLA, Lam Research, and Applied Materials increasingly run certified pre-owned and trade-in programs. These can offer credit against new purchases or refurbishment-backed resale, with the assurance of factory support. The trade-off is that OEM channels may not maximize cash and can favor the manufacturer’s commercial interests, so they are best evaluated against open-market alternatives rather than accepted by default.

Brokers, dealers, and digital marketplaces

Specialized brokers and dealers, alongside digital platforms such as Moov, CAE Online, fabsurplus, and SurplusGLOBAL, form the backbone of the open secondary market. SurplusGLOBAL’s launch of an AI-powered marketplace, SemiMarket, signals how the channel is professionalizing away from fragmented, relationship-only sourcing. Brokers add value through buyer networks and de-installation know-how; marketplaces add reach and price transparency. Many recovery programs use both, and the discipline of choosing channels mirrors the logic in our analysis of the strategic advantage of remarketing assets.

Auctions, internal redeployment, and responsible recycling

Auctions can be effective for full-line liquidations or where speed matters more than top dollar. Before any external sale, however, the first question should always be internal redeployment: can the tool move to another site, another node, or a sister facility? Redeployment captures the full embodied value with no resale discount. When a tool genuinely has no reuse path, responsible recycling, recovering precious and critical metals, becomes both the compliant and the sustainable choice. The trade-offs across auctions, direct sale, and recycling are the same ones covered in our broader guide to asset disposition.

Used semiconductor equipment disposition channels and the valuation drivers that determine net recovery.

The Sustainability Case for Reusing Semiconductor Equipment

Financial recovery is only half the value story. Reusing a semiconductor tool, rather than scrapping it and building a replacement, avoids an enormous amount of embodied carbon and material extraction. For sustainability and ESG leaders, fab tool reuse is one of the cleanest examples of circular value creation in heavy industry.

Embodied carbon and Scope 3 emissions

Every new capital tool carries embodied carbon from the energy, materials, and supply chain that built it. Extending the life of existing equipment avoids that footprint entirely. Research on refurbished technology more broadly finds reuse can substantially reduce carbon impacts when it displaces the purchase of new equipment, and the principle holds for capital equipment: the greenest tool is the one that already exists. Because purchased capital goods and end-of-life treatment both fall under Scope 3, recovery decisions show up directly in a corporate carbon inventory, a connection we unpack in our Scope 3 emissions reduction playbook.

Circular win: When a recovered tool is redeployed or resold instead of scrapped, the buyer avoids building new and the seller avoids disposal. One transaction, two carbon footprints reduced, and a financial return on both sides.

Circular economy and critical materials recovery

Semiconductor tools are dense with high-grade steel, specialty alloys, copper, and critical and precious metals. Reuse keeps that material in productive service; when reuse is exhausted, responsible recycling recovers the metals for new use. Recycled critical minerals carry on average roughly 80% less greenhouse gas than primary material from mining, according to the International Energy Agency. This is the circular economy in its most tangible form, and it connects fab recovery to the wider practice described in our circular economy asset management guide.

ESG reporting and disclosure value

Avoided emissions and diversion from landfill are increasingly reportable, decision-useful metrics. As disclosure expectations tighten, the ability to quantify the carbon and waste avoided through equipment reuse turns a recovery program into an ESG asset, not just a finance one. Building that measurement into an ESG-aligned asset lifecycle strategy turns recovery into a reportable sustainability outcome. Done well, investment recovery lets a company report both the dollars recaptured and the tons of carbon avoided in the same line item.

Building a Used Semiconductor Equipment Recovery Playbook

Strategy becomes value only through execution. A repeatable playbook for used semiconductor equipment turns each decommissioning from an improvised scramble into a controlled value-capture exercise. The three phases below scale from a single line shutdown to a full fab closure.

Plan disposition before the line goes dark

The most expensive mistake is treating disposition as an afterthought. The moment a line is flagged for retirement, recovery planning should begin: inventory and photograph assets while they are still installed and documented, capture run-hour and maintenance records before staff disperse, and obtain preliminary market valuations early. Tools that are de-installed carelessly or stored without documentation lose value fast. If your organization has no formal program yet, our step-by-step guide on how to start an investment recovery program is the place to begin.

Choose the right partner and channel mix

Few internal teams have the buyer networks, valuation depth, and logistics expertise that high-value fab tools demand. The right specialist partner brings all three, plus decontamination and de-installation capabilities. Evaluate partners on realized prices, transparency, environmental compliance, and global reach, then deliberately mix channels: OEM trade-in for some assets, brokered or marketplace sale for others, redeployment where possible, and recycling for the remainder. The goal is the highest total net recovery across the whole asset pool, not the highest price on any single tool.

| Disposition channel | Best for | Main trade-off |

|---|---|---|

| Internal redeployment | Tools with an active node match at another site | Relocation and reinstall cost; no cash inflow |

| OEM certified pre-owned / trade-in | Tools where factory support adds buyer confidence | May not maximize cash; favors OEM interests |

| Brokers and digital marketplaces | High-value tools needing reach and price discovery | Fees and commissions; longer sales cycle |

| Auction | Full-line liquidations where speed matters | Prices vary with auction-day demand |

| Responsible recycling | Tools with no reuse path; contaminated systems | Lowest financial return; strongest compliance and ESG fit |

Document, measure, and report ROI

What gets measured gets funded. Track realized recovery value against book value, the share of assets reused versus recycled, and the carbon and landfill diverted. Reporting both the financial and environmental return moves investment recovery from a back-office cleanup function to a strategic capability, and it makes the case for resourcing the next decommissioning properly. The discipline of measuring and remarketing is the same one detailed in our complete ITAD guide, applied to the highest-value tools your organization will ever retire.

Timing note for 2026: Under current law, the CHIPS Act advanced manufacturing investment credit (Section 48D) equals 35% of qualified investment in semiconductor manufacturing property, following a 2025 amendment that substituted “35 percent” for “25 percent” and applies to property placed in service after December 31, 2025 (26 U.S.C. §48D). One nuance matters for the secondary market: the statute requires that the original use of the acquired property commence with the taxpayer, so the credit primarily drives appetite for new tooling rather than used. Sellers who understand the buyer’s tax calculus can time and position assets to meet demand while it is strongest.

Frequently Asked Questions

Sources and References

- GlobeNewswire / Research and Markets, “Growth Opportunities in the $10.6 Billion Used Semiconductor Equipment Market, 2026-2030,” 2026. Market sizing ($4.55B in 2025 to $10.59B by 2030) and 18.3% CAGR. Link

- OpenPR, “Semiconductor Equipment Trading Market Forecast 2026-2032,” 2026. Broader trading market size to $17.75 billion. Link

- Resource Recycling (E-Scrap News), “What Intel’s blockbuster quarter means for ITAD,” April 2026. Intel excess-tool impairment and disposition context. Link

- Congressional Research Service, CHIPS Act provisions including Section 48D advanced manufacturing investment credit. Link

- U.S. Code, 26 U.S.C. §48D, Advanced Manufacturing Investment Credit. Credit equals 35% of qualified investment following the 2025 amendment; the original use of acquired property must commence with the taxpayer; applies to property placed in service after December 31, 2025. Link

- McKinsey & Company, “Sustainability in semiconductor operations: Toward net-zero production.” Industry decarbonization context. Link

- Lam Research, “Advancing Energy Efficiency in Semiconductor Manufacturing With Tool Upgrades.” Tool life extension and subsystem energy savings. Link

- International Energy Agency, on recycled critical minerals carrying roughly 80% lower greenhouse gas than primary material. Link

- SurplusGLOBAL, SemiMarket AI-powered used semiconductor equipment marketplace. Link

This article is published by the Investment Recovery Association (IRA) for educational and informational purposes only. It does not constitute legal, financial, or professional advice. Market data, statistics, and projections cited are sourced from third-party reports and are subject to change. Readers should consult qualified professionals before making business decisions based on the information presented. The IRA makes no warranties regarding the accuracy or completeness of third-party data referenced herein.