TL;DR

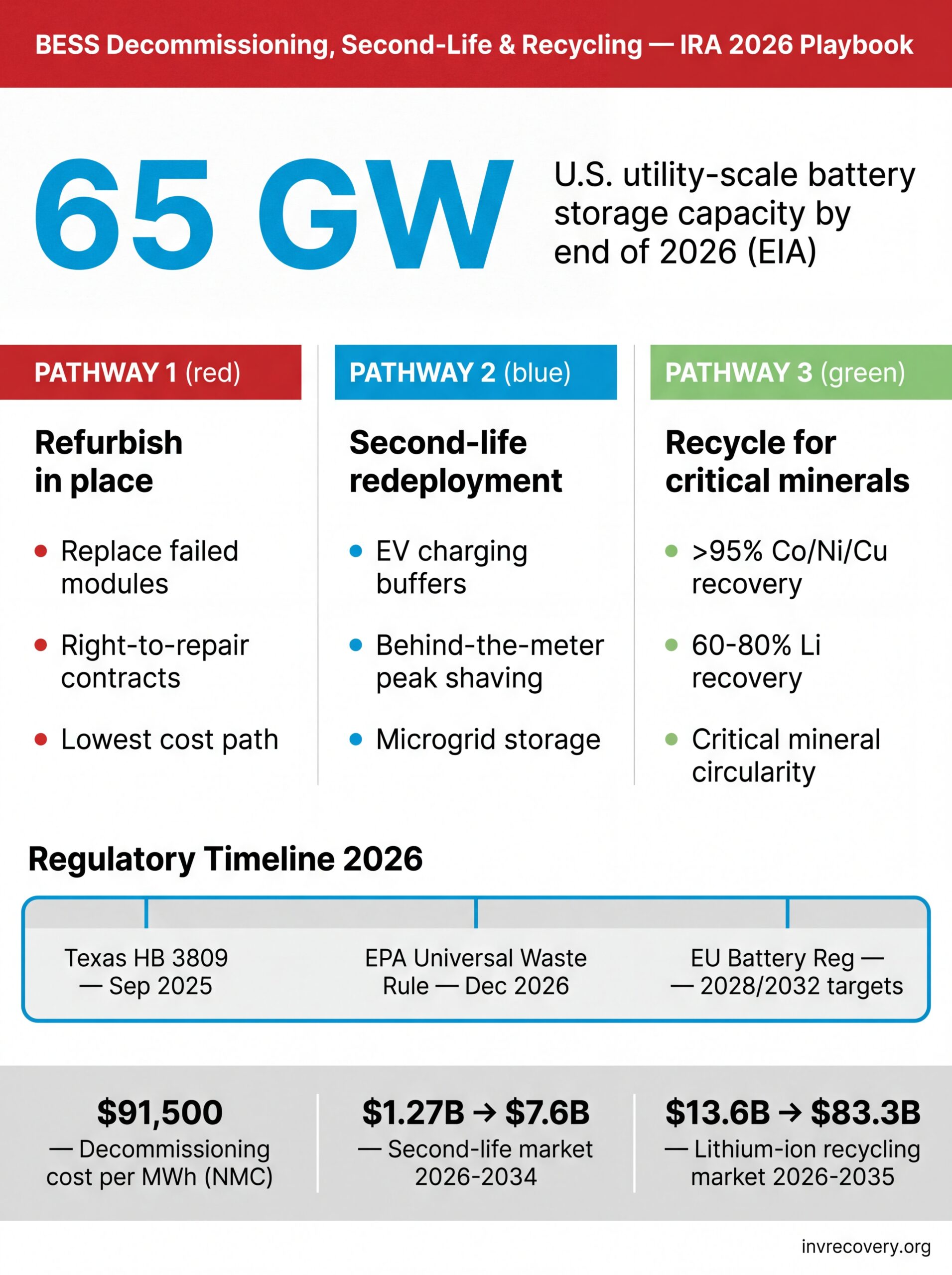

- The U.S. installed battery energy storage system fleet is on track to reach roughly 65 GW by the end of 2026, more than double its early-2025 level, which makes BESS end-of-life a near-term investment recovery priority, not a 2040 problem.

- Decommissioning a 1 MWh NMC lithium-ion battery energy storage system costs around $91,500, but up to 5.9% of original CapEx can be reclaimed through second-life redeployment, recycling credits, and critical-mineral recovery.

- Texas HB 3809 (effective September 1, 2025) is the first U.S. law to mandate BESS decommissioning, recycling, and financial assurance at the lease level, and the EPA’s pending universal-waste rule will tighten the screws nationally.

- The second-life battery market reached around $1.27–1.70 billion in 2026 and is projected to grow at 25–41% CAGR through the early 2030s, making second-life one of the highest-leverage moves an IR program can make this decade.

- IRA members can capture this opportunity now by building a three-pathway recovery framework (refurbish, second-life, recycle), aligning vendor contracts with state and federal end-of-life rules, and reporting outcomes inside their ESG disclosures.

Why Battery Energy Storage System Decommissioning Now Matters for Investment Recovery

The U.S. battery energy storage system buildout has moved from interesting niche to dominant grid asset class in less than four years. The Energy Information Administration projects that domestic utility-scale storage will rise from about 28 GW at the end of Q1 2025 to roughly 65 GW by the end of 2026, with developers planning 24 GW of new BESS additions in 2026 alone — up from a record 15 GW in 2025. For IRA members and corporate sustainability leaders, that growth curve has a hidden tail: every megawatt installed today is a megawatt that will need a recovery plan within ten to fifteen years. Battery energy storage decommissioning is no longer a hypothetical 2035 line item; it is a 2026 operational planning question.

Investment recovery teams already build playbooks for wind turbine decommissioning, oil and gas asset abandonment, and accelerated data center retirements. Lithium-based BESS deserves the same treatment. What is different here is timing: the first generation of grid-scale battery energy storage systems is now reaching the warranty cliff, and 2026 is the year the regulatory environment finally caught up with the deployment curve.

New utility-scale BESS capacity expected to come online in the U.S. in 2026, per the EIA — 60% above 2025’s record additions

What Is a Battery Energy Storage System, and What Actually Gets Decommissioned?

A battery energy storage system is an engineered package of lithium-ion (or, less commonly, sodium-ion or flow) battery modules, power conversion electronics, thermal management, fire suppression, and a control and communications stack. At scale, these battery energy storage systems (BESS) sit inside shipping-container-style enclosures and connect to the grid through transformers and switchgear. Most utility-scale projects today are best described as lithium-ion battery energy storage systems paired with renewable energy battery storage applications — solar firming, wind shaping, and standalone arbitrage being the most common. From an investment recovery standpoint, a BESS is not a single asset — it is a stack of assets with very different end-of-life economics:

- Battery modules and racks: the biggest line item on the asset register, the biggest safety risk at end of life, and the biggest second-life upside.

- Power conversion systems and inverters: often refurbishable and resellable independent of the battery itself.

- Transformers, switchgear, and balance-of-plant: reusable in other projects or recoverable for scrap-metal value, similar to the assets covered in our electric transformer recovery analysis.

- Container enclosures, foundations, cabling, and HVAC: straightforward to recover or recycle once the energized components have been removed safely.

Chemistry has shifted dramatically and that affects how you plan recovery. According to IRENA-cited data, LFP grew from 48% of the utility-scale battery market in 2021 to roughly 85% in 2024, while NMC fell from 36% to 9%. More than 90% of new BESS deployments now use LFP cells. LFP modules contain less cobalt and nickel than NMC, which makes them safer and cheaper to handle — but it also lowers the raw-material salvage value per ton. Recovery teams need to price both chemistries differently and avoid assuming what worked for early NMC systems will pencil out for an LFP retirement in 2032.

Key distinction: “End of life” for a BESS does not mean the cells are dead. Most utility-scale battery energy storage systems are retired from primary service when usable capacity drops to roughly 70–80% of nameplate — well above the threshold for a second-life application. That gap is where investment recovery value lives.

The Three Recovery Pathways for a Retired Battery Energy Storage System

An investment recovery decision for a BESS sits on the same decision tree that drives any asset disposition choice, with three viable pathways:

Pathway 1: Refurbish and Extend Service Life

Replace failed modules, refresh the battery management system, recommission the inverters, and keep the asset in primary service. This is usually the lowest-cost path when degradation is concentrated in a few modules rather than the full string. It is also the most underused option because OEM warranties and software licenses can lock out third-party refurbishers. Negotiating “right to repair” language into BESS procurement contracts up front is a major IR lever, comparable to how data center decommissioning programs negotiate vendor lock-out clauses.

Pathway 2: Redeploy as a Second-Life Battery

Pull the battery modules out of a high-cycle utility application and resell them into lower-stress use cases: behind-the-meter peak shaving, EV charging buffer storage, microgrids, telecom backup, and stationary storage at industrial sites. According to multiple market analyses, the global second-life battery market reached an estimated USD 1.27 billion in 2026 and is projected to expand at a 25.1% CAGR through 2034. Some bullish forecasts put the market at over USD 224 billion by 2040, implying a roughly 41% CAGR.

Pathway 3: Recycle for Critical-Mineral Recovery

Send the modules to a certified lithium-ion recycler for shredding, leaching, and metal recovery. The global lithium-ion battery recycling market reached USD 13.6 billion in 2026 and is forecast to grow at 22.3% CAGR to USD 83.3 billion by 2035. Leading recyclers now report greater than 95% recovery rates on cobalt, nickel, and copper, with lithium recovery in the 60–80% range and improving fast. That kind of mineral circularity is exactly the dynamic we map in our circular economy asset management guide.

Sustainability win: Recovering one ton of cathode material via lithium-ion battery recycling avoids tons of CO2e versus mining new ore and routes critical minerals back into U.S. domestic supply chains. That is real “sustainability heroism” in the language of green asset management ROI, and it is auditable.

Decommissioning Regulations Every BESS Asset Manager Should Track in 2026

For most of the past decade, BESS decommissioning lived in the regulatory gray zone. That ended in 2025. Three regulatory shifts now define the playing field:

Texas HB 3809 and the New Lease-Level Decommissioning Mandate

Signed by Governor Abbott in 2025 and effective September 1, 2025, Texas HB 3809 requires every battery energy storage system lease to obligate the lessee to remove all infrastructure (battery units, transformers, substations, buried cable), recycle or reuse what is recyclable, and post financial assurance before the earlier of the lease termination date or the 15th anniversary of the battery’s operation date. That is a hard, contractual deadline for IR planning — not a soft sustainability goal. Other states are watching the Texas template closely.

EPA’s Universal Waste Rule for Lithium Batteries

The EPA has signaled that a federal universal-waste rule for lithium-ion batteries and solar panels will move forward, with a proposed rulemaking targeted for 2025 and final adoption expected by December 2026. The rule is designed to cut fire risk during transport and storage and to harmonize state-by-state lithium-battery waste handling. Once finalized, it will affect every IR program that handles batteries through reverse logistics, mirroring the kinds of compliance shifts we tracked in our tariff and trade-policy analysis.

EU Battery Regulation and the Global Knock-On Effect

The 2023 EU Battery Regulation sets minimum recovered-content targets that ratchet up over time: 90% recovery for cobalt, copper, and nickel and 50% for lithium by 2028, rising to 95% and 80% respectively by 2032. Multinational asset owners with EU operations need recovery contracts that can document chain-of-custody and recovered-mineral percentages, not just “we recycled it.” That documentation requirement quietly raises the bar for every U.S. BESS recovery program selling into multinational supply chains.

The 2026 BESS investment recovery playbook at a glance: pathway selection, cost benchmarks, regulatory triggers, and sustainability impact.

Building a BESS Investment Recovery Playbook: A Five-Step Roadmap

The most successful BESS recovery programs follow a structured process that looks a lot like the playbook we describe in What Is Investment Recovery? The Complete 2026 Guide. Adapted to lithium-ion stationary storage, the workflow looks like this:

Step 1: Asset Audit and State-of-Health Benchmarking

Before deciding what to do with a retired battery energy storage system, you need to know what is actually in it: chemistry, cell vendor, module count, original nameplate energy, current state of health, cycle history, and any safety incidents on record. This audit feeds every downstream decision. For older fleets, the audit also flags whether you have NMC modules with materially higher cobalt content (and higher salvage value) or LFP modules with lower per-ton value but easier handling.

Step 2: Pathway Decision Matrix

Score each battery string on three axes: (1) remaining usable capacity, (2) safety incident history, and (3) cost to refurbish per kWh. High capacity plus clean safety record points to refurbishment in primary service. Mid-range capacity plus clean record points to second-life redeployment. Anything with safety incidents or sub-50% capacity goes straight to certified recycling.

Step 3: Vendor Selection and Contracting

Build a shortlist of three to five qualified vendors per pathway: refurbishment specialists, second-life integrators, and certified lithium-ion recyclers. Verify ESG-aligned credentials — ISO 14001, R2v3, e-Stewards, and (for EU exposure) compliance with the Battery Regulation’s traceability rules. Negotiate revenue-share or rebate clauses where second-life or recovered-mineral value exists.

Step 4: Safe De-energization, Transport, and Chain of Custody

Lithium-ion modules are universally treated as hazardous goods in transport. Plan for state-of-charge reduction before shipment, certified hazmat carriers, and PHMSA-compliant packaging. Documentation matters: a chain-of-custody record from de-energization to final disposition is the audit trail your ESG team will need.

Step 5: Financial Reconciliation and Reporting

Capture every dollar of recovered value — refurbishment cost avoidance, second-life sale proceeds, recycling rebates, transport-cost offsets — and report it inside the same framework you use for other surplus categories. The goal is to close the loop with your finance team and your ESG team in one set of numbers.

Second-Life Economics: Where the Real Investment Recovery Upside Sits

For most retired utility-scale battery energy storage systems, second-life redeployment delivers a larger net present value than either refurbishment or immediate recycling. The reason is straightforward: a retired BESS still has 70–80% of its original usable capacity, and there are large, growing markets that will pay for it.

Applications that are working today include EV fast-charging buffer storage (which smooths out grid demand and avoids costly utility upgrades), behind-the-meter peak shaving for industrial customers, microgrid integration on remote sites, and standby storage for telecom and data center backup. Our EV battery recycling playbook covers the parallel mobility-to-stationary path; the BESS-to-BESS second-life path is similar in structure but operates at much larger module sizes.

The economics get more interesting when you factor in the second-life market’s growth. With CAGRs in the 25–41% range and total addressable market estimates in the tens of billions of dollars by the early 2030s, IR programs that lock in long-term offtake relationships with second-life integrators today will be positioned for outsized recovery returns later in the decade.

| Recovery Pathway | Best For | Typical Net Recovery Value | Sustainability Impact |

|---|---|---|---|

| Refurbish in place | Low cycle count, isolated module failures | Highest (avoided replacement CapEx) | Highest carbon avoidance per kWh |

| Second-life redeployment | 70–80% remaining capacity, clean safety record | High (sale proceeds + extended useful life) | High (delays new cell manufacturing) |

| Recycling for minerals | End-of-second-life, safety-flagged, sub-50% capacity | Moderate (rebates + scrap value) | Strong (90%+ critical-mineral recovery) |

Sustainability, ESG, and the Story Behind the Numbers

BESS recovery is not just a financial play. It is one of the cleanest sustainability stories an investment recovery program can tell because the numbers are quantifiable and externally verifiable. Every retired utility-scale battery energy storage system that gets a second life delays the manufacture of an equivalent new system, and the embodied carbon savings are large. Every ton of cathode material recovered through certified recycling cuts mining-related carbon emissions and routes critical minerals back into domestic supply chains.

For ESG reporting, BESS recovery maps cleanly into SASB, CSRD, and IFRS S2 frameworks. The metrics that typically matter are: percentage of retired BESS capacity diverted from disposal, percentage of critical minerals recovered, Scope 3 emissions avoided through second-life redeployment, and total dollar value recovered. IR teams that report these alongside their broader renewable-asset recovery numbers are increasingly being asked to present at the board level.

Frequently Asked Questions

Sources and References

- U.S. Energy Information Administration, “U.S. utility-scale energy storage to double, reach 65 GW by 2027,” 2025 — capacity projections cited in Utility Dive coverage. link

- U.S. Energy Information Administration, “New U.S. electric generating capacity expected to reach a record high in 2026” — 2026 BESS additions and geographic concentration. link

- Baker Botts L.L.P., “Texas Adopts New Decommissioning Law for Battery Energy Storage Systems,” 2025 — HB 3809 analysis. link

- U.S. EPA, “Improving Recycling and Management of Renewable Energy Wastes: Universal Waste Regulations for Solar Panels and Lithium Batteries” — pending federal rulemaking. link

- InsideEVs, “Why LFP Became The Dominant EV Battery Chemistry In 2025” — LFP vs. NMC market share for utility-scale BESS (IRENA-cited data). link

- Fortune Business Insights, “Second Life EV Battery Market Size, Share & Growth,” 2026 — second-life market size and CAGR. link

- OpenPR / Lithium-Ion Battery Recycling Market Forecast 2035 — recycling market size $13.6B in 2026, $83.3B by 2035, 22.3% CAGR. link

- Green-Clean Solar, “Recycling of Utility-Scale Battery Storage Systems” — per-MWh decommissioning cost benchmark for NMC systems. link

- U.S. EPA, “Solar Panel and Lithium Battery Universal Waste Proposed Rule” briefing materials — federal universal-waste timeline. link

- Yahoo Finance / Research and Markets, “Second Life EV Battery Markets, 2026-2040” — bullish $224B-by-2040 second-life forecast. link

Disclaimer: This article is published by the Investment Recovery Association (IRA) for educational and informational purposes only. It does not constitute legal, financial, or professional advice. Market data, statistics, and projections cited are sourced from third-party reports and are subject to change. Readers should consult qualified professionals before making business decisions based on the information presented. The IRA makes no warranties regarding the accuracy or completeness of third-party data referenced herein.