TL;DR

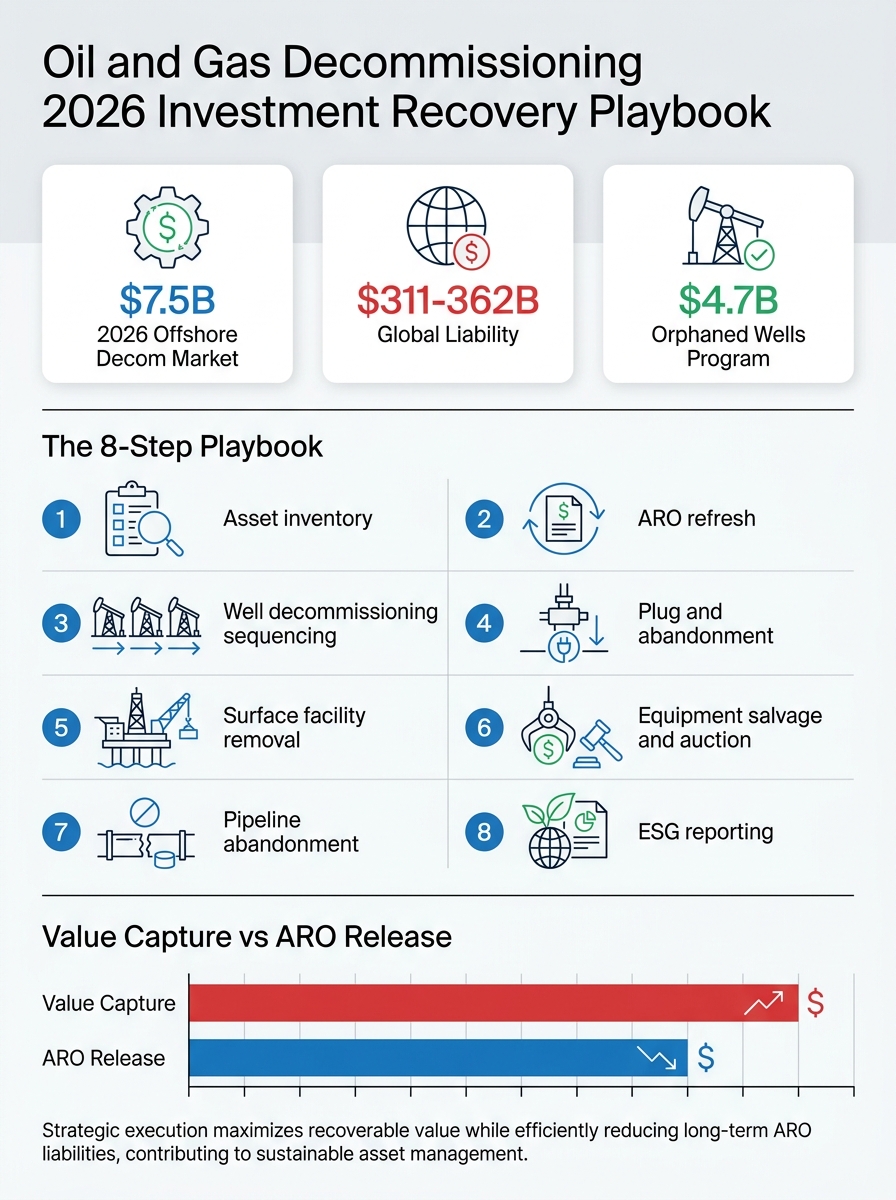

- Oil and gas decommissioning is a $7.5B market in 2026 growing at roughly 8% CAGR, with global liability now estimated at $311-362B — investment recovery teams own a defining slice of that conversation.

- Well abandonment, plug and abandonment, and pipeline abandonment are no longer purely engineering tasks; they sit at the intersection of asset retirement obligation accounting, ESG reporting, and value capture from oilfield equipment auctions.

- Federal funding has accelerated the timeline: the $4.7B Bipartisan Infrastructure Law orphaned wells program has already plugged 9,500+ wells and queued 10,000+ more across 24 states.

- Use our 8-step playbook to turn end-of-life upstream assets into measurable recovery, defensible compliance, and a credible methane reduction story.

Why Oil and Gas Decommissioning Is a 2026 Investment Recovery Priority

Oil and gas decommissioning has moved from an obscure accounting footnote to a defining issue for upstream operators, midstream owners, and the investment recovery teams who report to them. In 2026, the global offshore decommissioning market alone is projected to reach about $7.5 billion and grow at roughly 8% CAGR through the early 2030s, while the present value of worldwide oil and gas decommissioning liability sits between $311 and $362 billion. Add the onshore U.S. orphaned wells program and the picture is unambiguous: this is the largest planned asset retirement wave the industry has ever managed.

For investment recovery (IR) professionals, that wave is both a compliance challenge and a value opportunity. Every retired wellhead, separator, compressor train, and length of tubing is a node on a value chain that includes sustainable asset recovery, ARO release, scrap and tubular markets, and Scope 3 reporting. Teams that run this work as a structured program, similar to the aircraft retirement and parts recovery playbook or the wind turbine decommissioning playbook, consistently outperform peers who treat decommissioning as a one-off cost event.

This 2026 playbook covers the financial, regulatory, operational, and sustainability levers your IR team should be pulling. It is written for investment recovery managers, supply chain leaders, sustainability directors, and asset disposition specialists who carry the responsibility for moving billions of dollars in retired upstream assets through the door at the highest possible net recovery.

A $7.5B offshore decommissioning market and growing

Multiple market research firms put the offshore segment between $7.24B and $9.07B in 2026, with CAGRs of 4.78% to 8.38% depending on methodology. Europe leads on activity ($4.52B in 2026), driven by North Sea maturity, while the U.S. Gulf of Mexico, Asia Pacific, and Latin America are all scaling rapidly. Globally, roughly 2,600 platforms are forecast to need decommissioning by 2040 at a total cost of approximately $210 billion.

Aging wells, tightening rules, and a closing window to capture salvage value

Onshore the story is similar. U.S. regulators estimate more than 15,000 orphaned wells on federal land alone, plus tens of thousands more on state and private leases. As wells age past their economic life, operators face a choice: keep paying integrity-management costs, or commit to well decommissioning with a clear investment recovery plan. Salvage value erodes quickly once equipment sits exposed, so the IR team’s ability to move fast on equipment harvest is the difference between meaningful recovery and pennies on the dollar.

From cost center to value engine: the IR lens on retirement

The biggest mindset shift in 2026 is treating oil and gas decommissioning as an investment recovery program rather than a closing checklist. That means the IR team is in the room from end-of-life triage, not just at the auction stage. It means ARO liability releases, scrap and oilfield equipment auction proceeds, and avoided integrity spend are reported together. And it means recovered tubing, compressors, separators, and structural steel flow into circular economy in investment recovery channels that align with corporate sustainability commitments.

Present value of global oil and gas decommissioning liability (2022 estimate, IEA / industry analyses)

Inside the Numbers: ARO, Salvage Value, and the Funding Gap

Every credible oil and gas decommissioning conversation in 2026 starts with the balance sheet. Under FASB ASC 410-20, operators must record an asset retirement obligation (ARO) at fair value when a legal obligation to retire a long-lived asset is incurred. That liability accretes over time, the asset side capitalizes the retirement cost, and IR teams operate against the difference between the booked ARO and the real-world net of execution cost minus recovered value.

Global decommissioning liability now $311-362B

The headline number is huge, but it understates what is coming. Offshore decommissioning costs alone are estimated at about $10.4 per barrel of oil equivalent in low-cost scenarios, and they rise sharply in deep water. The U.S. GAO has flagged that the Department of the Interior holds only about $3.5 billion in bonds against potential offshore obligations of $40-70 billion, an exposure gap regulators are actively closing through new financial assurance rules.

Asset retirement obligation (ASC 410-20) and IR oversight

IR involvement strengthens ARO accuracy. By feeding current oilfield equipment auction prices, scrap benchmarks, and realistic teardown timelines back into the engineering and accounting teams, IR managers help shrink the variance between booked liability and actual cash-out. That work matters because lenders, rating agencies, and acquirers scrutinize ARO disclosures during M&A and refinancing events. A defensible ARO with documented IR assumptions de-risks transactions.

$40-70B exposure vs. $3.5B in bonds: why IR teams own this conversation

The funding gap also reframes the IR team’s seat at the table. CFOs and audit committees are asking sharper questions about retirement readiness, especially for legacy fields and platforms approaching end-of-life. IR teams that can quantify net recovery, surface salvage assumptions, and tie execution to ESG outcomes become essential advisors, not back-office processors. This is the same arc we saw with EV battery investment recovery playbook work, where IR leadership now shapes capital allocation, not just disposal.

Orphaned Wells, Federal Funding, and the New Oil and Gas Decommissioning Compliance Reality

Onshore U.S. oil and gas decommissioning has been transformed by federal money. The Bipartisan Infrastructure Law dedicated $4.7 billion to plug, remediate, and reclaim orphaned wells, the largest investment in legacy pollution cleanup in American history. That program is now four years into execution and reshaping how operators and contractors plan abandonment work.

$4.7B Bipartisan Infrastructure Law program

The Department of the Interior has awarded an initial $560 million to 24 states under the program, with additional formula and performance grants totaling hundreds of millions more. Federal land contracts go through the BLM, while state programs handle private-land wells. Since the law’s enactment, states have plugged nearly 9,500 orphaned wells and queued thousands more.

10,000+ wells in queue across 24 states

For IR teams, the orphaned wells push has three immediate effects. First, it absorbs service company capacity, tightening the contractor market for operator-led well plugging. Second, it raises the public profile of plug and abandonment quality, since orphaned-well failures are now scrutinized politically. Third, it normalizes documentation, traceability, and methane verification, which carry over to corporate decommissioning programs.

What IR managers should track in their well portfolio

At a minimum, an IR manager overseeing oil and gas decommissioning should be able to answer six questions about every shut-in or end-of-life well: when did production stop, what is the current integrity status, what is the latest ARO estimate, what equipment is still salvageable, who is the preferred plug and abandonment contractor, and what is the estimated net recovery. If those numbers do not exist as a portfolio view, the IR team has work to do before any auction or contractor RFP goes out.

Definition check: Well abandonment and plug and abandonment (often shortened to “P&A”) refer to permanently sealing a well to prevent migration of fluids between formations and to the surface. Well decommissioning is the broader retirement scope that includes P&A plus surface equipment removal, site restoration, and regulatory close-out.

The 8-Step Oil and Gas Decommissioning Playbook

This 8-step sequence works for a single platform retirement, a basin-wide well decommissioning program, or a midstream pipeline abandonment. Adjust the depth at each step to match your asset class, but do not skip steps. Most cost overruns trace back to either Step 1 or Step 6.

Step 1: Asset inventory and end-of-life triage

Build the master list. For each wellbore, platform, compressor station, or pipeline segment, capture location, age, current status, last integrity inspection, booked ARO, and a preliminary classification: keep producing, shut-in with monitoring, prep for decommissioning, or already eligible. This is the single most important document in the program and it lives with the IR team alongside engineering. Borrow process discipline from the data center decommissioning checklist; it travels well across industries.

Step 2: ARO refresh and IR sign-off

Update the asset retirement obligation for each asset entering the decommissioning queue using current contractor rates, scrap prices, and oilfield equipment auction comps. Sign-off should be joint between IR, asset management, and accounting. This is also the moment to tag which assets carry meaningful salvage value worth pre-positioning for harvest.

Step 3: Well decommissioning sequencing

Sequence wells by basin proximity, contractor availability, regulatory windows, and salvage logistics. Clustering wells in a single mobilization window cuts unit P&A cost dramatically. Where possible, align with pipeline abandonment and surface facility removal so contractors can chain the work.

Step 4: Plug and abandonment execution

Plug and abandonment is the regulated heart of well decommissioning. Cement plugs are set to isolate hydrocarbon zones, freshwater aquifers, and the surface; tubing is recovered where possible; the wellhead is cut and capped. Quality control here protects the operator from future methane emissions, regulatory action, and orphan-well reclassification. IR’s role is to make sure recovered tubular and wellhead steel flows into the salvage stream, not the rental return pile.

Step 5: Surface and facility decommissioning

Tanks, separators, compressors, generators, instrumentation, piping, structural steel: all of it needs an IR plan. Sort assets into three buckets: redeploy within the company, sell as functional units, or dismantle for scrap. Documentation is critical because some equipment will require evidence of provenance and integrity to enter the resale market.

Step 6: Oilfield equipment salvage and auction

This is where IR’s expertise drives the biggest delta. The choice between an oilfield equipment auction, a brokered private sale, a competitive bid to an aftermarket buyer, or scrap merchant depends on equipment type, condition, location, and timing. A single well-run auction event tied to a platform retirement or basin exit can recover seven figures that would otherwise be lost.

Step 7: Pipeline abandonment and site restoration

Pipelines are often the last asset class to be addressed, but they carry meaningful recovery potential in steel value, plus growing scrutiny on methane and product-line cleaning. Decide segment-by-segment between abandonment-in-place and full removal based on environmental sensitivity, salvage value, and regulator preference. Restore the surface to permit conditions.

Step 8: ESG reporting and lessons learned

Close out every retirement event with a single dashboard: tonnes of steel recovered and recycled, tonnes of methane avoided, ARO release, net recovery vs. plan, and Scope 3 implications. Feed those numbers back into the next sequencing cycle. This is the same loop described in the 8 steps to grow your IR program framework.

The 2026 oil and gas decommissioning playbook: 8-step workflow, ARO mechanics, and the orphaned wells funding picture at a glance.

Maximizing Recovery from Oilfield Equipment Auctions and Salvage

The oilfield equipment auction market is deep, global, and historically opaque, which is exactly the environment where a disciplined IR team can outperform. Platforms like Salvex (a $5.2B asset recovery marketplace), SalvageSale, Quipbase, and Oilpatch Surplus give IR teams visibility into comparable transactions, and traditional auctioneers like IronPlanet and EquipNet still drive premium results for well-prepared events.

Where the value lives: pumps, separators, compressors, tubulars

In a typical upstream retirement, the largest single-line recoveries come from gas compressors, treaters and separators, electric submersible pumps, glycol and amine units, generator sets, and high-grade tubular goods. Structural steel from platforms, while heavy, generally moves at scrap rather than aftermarket rates. Specialty items like cranes, helideck modules, and instrumentation are highly variable and benefit from individualized marketing.

Auction vs. broker vs. direct resale

Auction is usually right when you have a critical mass of equipment in one location, a clear deadline, and confidence that buyers will compete. Broker sales suit specialty items with a narrow buyer pool. Direct resale is right when an internal sister business unit or known buyer needs the exact asset. The same trade-off logic that informs industrial equipment liquidation applies to oilfield assets, with the added wrinkle that hazardous-area certifications can either dramatically boost or completely block resale value.

Tubular recovery and structural steel benchmarks

Tubular recovery is a recurring conversation in well plugging programs. Operators who recover and remarket OCTG (oil country tubular goods) cleanly can capture meaningful value, particularly during periods of tariff-driven steel inflation. Our 2026 tariff impact on surplus assets analysis lays out how trade policy shifts the math for steel-heavy retirement classes.

Offshore Decommissioning and Oil Rig Decommissioning Specifics

Offshore decommissioning and oil rig decommissioning concentrate the highest absolute costs and the most complex IR decisions. The economics of platform removal change radically with water depth, regulator, and rig type. The same value-recovery principles apply, but the execution requires marine specialists and far more lead time.

Platform removal economics by water depth

Public BSEE data shows that platforms in 122-250 meter water depths in the U.S. Gulf of Mexico run roughly $4.8 million per structure to remove, while 250-500 meter platforms range $10-80 million. Deepwater facilities go higher still. These numbers should anchor every offshore ARO review and every conversation with the IR team about realistic salvage offsets.

Subsea infrastructure and pipeline abandonment

Subsea infrastructure presents its own challenges. Trees, manifolds, flowlines, and umbilicals all carry recovery potential, but the cost of recovery is high. Many operators are running side-by-side comparisons of full removal vs. partial removal vs. abandonment in place, with the decision driven by environmental sensitivity, regulator preference, navigational risk, and salvage economics.

Rigs-to-reefs and partial removal options

Rigs-to-reefs programs in the U.S. Gulf of Mexico convert retired platforms into permanent artificial reefs, splitting the cost savings between operator and state. They are not available in every basin, but where they are, they can dramatically reduce decommissioning cost while contributing to marine biodiversity. IR teams should engage these conversations early so the salvage program is aligned to the chosen removal strategy.

Sustainability lens: Well-executed oil and gas decommissioning is one of the most direct ways the upstream sector can cut fugitive methane, recover thousands of tonnes of steel and copper for the circular economy, and deliver a credible Scope 3 narrative. IR teams are central to that story.

ESG, Methane, and Scope 3: The Sustainability Case

The strongest pitch for treating oil and gas decommissioning as an investment recovery program rather than a closing checklist is the sustainability story it tells. Scope 3 emissions can represent up to 80% of an oil and gas company’s footprint, and decommissioning sits inside Category 5 (waste generated in operations) and Category 12 (end-of-life treatment) of the GHG Protocol.

Methane abatement from proper well plugging

Improperly abandoned wells are a documented methane source. Tight, verified plug and abandonment work converts a contingent emissions liability into a defensible avoided-emissions claim. Combined with leak detection and repair programs, abandonment quality is one of the cheapest emissions reductions an operator can buy.

Scope 3 reporting tied to decommissioning

Standards alignment matters. The GHG Protocol and Ipieca’s petroleum-industry Scope 3 methodology both expect operators to account for end-of-life treatment of sold and own-use assets. IR teams that report tonnes diverted from landfill, tonnes returned to functional reuse, and tonnes recycled give the sustainability team auditable numbers to feed into corporate disclosures.

Circular-economy reporting for steel and copper recovered

Beyond carbon, the circular-economy story carries real weight with investors. Recovered carbon steel, stainless, copper wiring, aluminum, and brass instrumentation all feed back into industrial supply chains. For operators that have committed to circular sourcing targets, decommissioning recovery is a direct contributor.

Common Oil and Gas Decommissioning Pitfalls

Four mistakes show up repeatedly in retirement programs and account for the majority of cost overruns and salvage shortfalls.

First, treating decommissioning as a single closeout event rather than a multi-year program. Operators who plan retirement in isolation from production decline curves leave money on the table at every stage. The start an investment recovery program framework explicitly addresses how to fold retirement planning into the standard IR cadence.

Second, underestimating contractor lead times. The orphaned wells program plus a wave of operator-led plug and abandonment work has tightened service capacity in many basins. Booking contractors 12-18 months out is now common; waiting until the field is dead is expensive.

Third, harvesting too late. Equipment exposed to weather, salt air, or vandalism loses value quickly. Build a pre-mobilization sweep into the playbook so anything with resale value is harvested before site decommissioning crews arrive.

Fourth, ignoring the ESG narrative. Decommissioning done well is a sustainability story that investors and regulators want to hear. The IR team that captures the tonnage, methane, and circularity numbers in real time gives the company a competitive edge in disclosures.

Frequently Asked Questions

Sources and References

- Fortune Business Insights, Offshore Decommissioning Market Size, Share, Growth [2034]. Market size, CAGR, regional split.

- U.S. Department of the Interior, Bipartisan Infrastructure Law Orphaned Wells Program. Federal funding and state awards.

- U.S. Government Accountability Office, Offshore Oil and Gas: Interior Needs to Improve Decommissioning Enforcement (GAO-24-106229), 2024. Bonding gap.

- BSEE, Decommissioning Cost Estimates Online Query. Per-platform cost ranges.

- Resources for the Future, Decommissioning Orphaned and Abandoned Oil and Gas Wells: New Estimates and Cost Drivers, 2024.

- Norton Rose Fulbright, Sustainable Offshore Platform Decommissioning. Rigs-to-reefs and partial removal.

- Ocean Conservancy, Offshore Oil and Gas Decommissioning. Environmental considerations.

- FASB, ASC 410-20 Asset Retirement Obligations. Recognition and measurement guidance for upstream operators.

- Salvex, SalvageSale, Quipbase marketplace listings. Auction comparables for oilfield equipment.

This article is published by the Investment Recovery Association (IRA) for educational and informational purposes only. It does not constitute legal, financial, or professional advice. Market data, statistics, and projections cited are sourced from third-party reports and are subject to change. Readers should consult qualified professionals before making business decisions based on the information presented. The IRA makes no warranties regarding the accuracy or completeness of third-party data referenced herein.