TL;DR

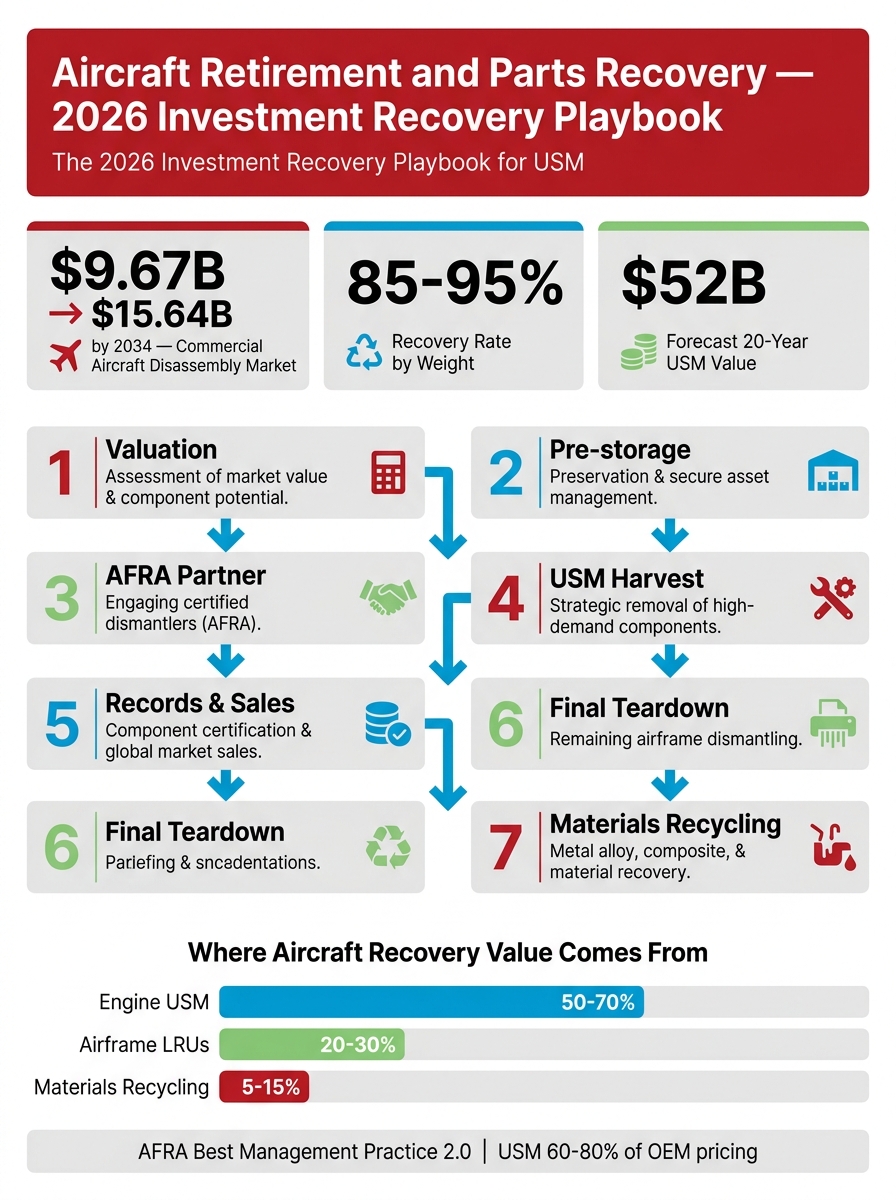

- The commercial aircraft disassembly and recycling market is on track to grow from $9.67B in 2026 to $15.64B by 2034 (6.20% CAGR), and Airbus forecasts roughly $52B in used serviceable material (USM) value over the next two decades.

- Aircraft recycling can return up to 85-95% of an airframe by weight back to productive use, with engine teardown alone accounting for about 40% of recovered part value.

- AFRA-accredited aircraft recycling companies follow Best Management Practice (BMP) guides for safe, traceable disassembly, which is the gating requirement for procurement, insurers, and regulators.

- A 7-step retirement playbook (valuation, parking, partner selection, USM harvest, parts sales, final teardown, materials recycling) is now table-stakes for investment recovery teams managing aging fleets.

- USM parts sell for 60-80% of new OEM pricing, making aircraft retirement a measurable ROI lever and a scope-3 emissions reduction story for sustainability reporting.

Why Aircraft Recycling Is a 2026 Investment Recovery Priority

Aircraft recycling has moved from a niche aviation aftermarket topic to a board-level investment recovery conversation. Post-pandemic fleet restructuring, the rising operating cost of older narrowbodies and widebodies, and the booming demand for used serviceable material (USM) have flooded the market with airframes ripe for disassembly. For investment recovery and corporate asset management teams, that is a once-in-a-cycle ROI opportunity that also delivers significant sustainability gains.

The market data backs this up. The global commercial aircraft disassembly, dismantling and recycling market reached USD 9.67 billion in 2026 and is projected to reach USD 15.64 billion by 2034, growing at a 6.20% CAGR. The parallel USM market is on a similar trajectory, rising from $7.64B in 2025 to $10.86B by 2033. Airbus’s most recent Global Services Forecast estimates that aircraft dismantling and recycling will generate roughly $52 billion in USM value over the next twenty years.

For investment recovery professionals, this is the same playbook that has reshaped wind turbine blade recycling and EV battery investment recovery: a fleet of high-value assets reaching end-of-life faster than anyone modeled, an aftermarket that is willing to pay strong recovery prices for serviceable components, and a regulatory and ESG environment that rewards traceable, certified recycling.

Definition: Aircraft recycling is the structured end-of-life process of harvesting reusable parts (USM), dismantling the airframe, and recovering raw materials such as aluminum, titanium, copper, and composites for productive reuse. AFRA-accredited operators report total mass recovery rates of up to 85-95% per aircraft.

Inside the Aircraft Recycling and USM Economics

The economics of aircraft recycling are stronger than most asset managers realize. Three forces are driving the curve.

1. USM demand is structural, not cyclical

USM parts typically sell at 60 to 80 percent of the price of a comparable new OEM component, and that price discipline is what airlines and MROs need to manage maintenance budgets. With engine overhauls now costing several million dollars per shop visit and lead times for new spare parts still elongated, certified USM has shifted from an opportunistic cost-saving lever to a strategic procurement category.

Estimated USM value generated by aircraft dismantling and recycling over the next 20 years (Airbus Global Services Forecast 2024-2043)

2. Recovery rates are exceptional

AFRA-accredited aircraft recycling companies report total recovery rates of up to 85 to 95% of an aircraft by weight. That includes aluminum airframe structures, titanium engine components, copper wiring, glass and composite materials, plus all of the line-replaceable units (LRUs) that go back into the aftermarket as USM. Compared to other heavy-asset end-of-life categories, aircraft sit at the high end of the recoverability spectrum.

3. Engine teardown drives the economics

In 2025, engine USM led the market with a 40.20% share due to the high demand for engine replacements and overhauls, which account for a significant portion of airline maintenance expenditure. For investment recovery teams, that means engine teardown is the single biggest value lever in any aircraft retirement program. Choosing whether to teardown, lease, or sell an engine as a green-time asset is the highest-impact decision in the retirement playbook.

AFRA Best Management Practices and Aircraft Recycling Companies

The Aircraft Fleet Recycling Association (AFRA) is the international non-profit that sets the bar for safe, traceable, environmentally responsible aircraft disassembly and recycling. AFRA’s Best Management Practice (BMP) guide, now in version 2.0, is the most widely referenced standard in the industry and the de facto procurement requirement for any major operator entering an aircraft retirement program.

AFRA offers accreditation across two pillars: Airframe and Engine Disassembly, and Aircraft Materials Recycling. Accreditation tells regulators, insurers, lessors, and procurement teams that the operator’s processes have been audited against the BMP. It is conceptually similar to how R2v3 and e-Stewards ITAD certifications govern responsible electronics recycling, just adapted to the aviation lifecycle.

What to look for when shortlisting aircraft recycling companies

| Capability | What good looks like | Red flags |

|---|---|---|

| AFRA accreditation | Current accreditation in disassembly and/or materials recycling, verifiable on AFRA’s site. | Lapsed accreditation or self-declared compliance with no audit trail. |

| Records and traceability | Complete back-to-birth traceability for high-value LRUs, with airworthiness event flags. | Bulk-removal language, no per-part documentation, no airworthiness history. |

| Mass-balance reporting | Mass-balance report by material stream (aluminum, titanium, composites, copper, hazardous). | Single “recycling rate” headline number with no breakdown. |

| USM marketing reach | Direct aftermarket distribution and digital marketplace access (e.g., aviation aftermarket platforms). | Reliance on a single broker, no marketplace presence, no auction option. |

This is the same procurement diligence pattern that tech-driven surplus asset strategies apply in IT and industrial categories. The certification is necessary but not sufficient; what matters is the operator’s ability to convert your retired fleet into documented, marketable USM with a defensible sustainability story.

The 7-step aircraft retirement and parts recovery playbook, mapped to recovery rates and projected USM value.

The 7-Step Aircraft Retirement and Disassembly Playbook

Whether you are retiring a single corporate jet, an end-of-lease widebody, or a fleet of narrowbodies, the underlying playbook is the same. The variables are scale, contract structure, and sustainability reporting depth.

Step 1: Valuation and end-of-life decision

Start with a market valuation that distinguishes the aircraft’s parted-out value (engines, APUs, landing gear, avionics, interior assets) from its flying value (lease extension, sale to a freighter converter, secondary operator). For older aircraft with high-time engines, the parted-out value is now frequently higher than the flying value, which is one of the structural drivers of the current dismantling boom.

Step 2: Pre-storage and parking

Once retirement is approved, the aircraft is parked in a desert storage facility, preserved per OEM procedures, and inventoried. This stage protects the value of engines and LRUs and gives the asset owner time to run a competitive teardown RFP rather than make a distressed-sale decision. Many of these facilities are colloquially known as boneyards, and they have evolved into sophisticated asset preservation and remarketing hubs.

Step 3: AFRA-certified partner selection

Shortlist three to five AFRA-accredited aircraft recycling companies. Request itemized USM recovery forecasts, mass-balance reporting templates, and references from comparable airframe types. This step mirrors how a new investment recovery program is built: the partner selection determines 70% of the eventual recovery economics.

Step 4: Asset stripping and USM harvest

Engines, APU, landing gear, avionics, in-flight entertainment, galleys, seats, and other high-value LRUs are removed in sequence, tagged with airworthiness records, and routed to USM marketing or direct sale channels. This is the highest-margin phase of the playbook; getting the documentation right is what unlocks aftermarket pricing.

Step 5: Records, traceability, and parts sales

USM parts move through certified distribution platforms or via auction. Buyers (airlines, MROs, brokers, parts pools) demand back-to-birth traceability and airworthiness compliance. The strength of your records package is directly correlated to the price each part will fetch. Aircraft auction online platforms have also reduced search costs for buyers and broadened the global bidder pool, which has historically lifted realized prices.

Step 6: Final dismantling and aircraft salvage

After USM harvest, the remaining hulk moves into final dismantling. Aluminum, titanium, copper, and steel are segregated and sold by stream. Composites, batteries, hydraulic fluids, and hazardous materials are processed per the AFRA BMP. This is the stage that classic aircraft salvage language refers to, but in practice it is a controlled materials recovery process rather than a scrapyard activity.

Step 7: Materials recycling and sustainability reporting

Material streams go to qualified recyclers. The asset owner receives a mass-balance report quantifying how much material was recycled, reused, and landfilled, plus an estimate of CO2 emissions avoided versus virgin-material production. That report drops directly into ESG and sustainability disclosures, in the same way that a data center decommissioning checklist produces audit-ready evidence for scope-3 reporting.

ROI: How Aircraft Disposal Companies Maximize Recovery

Recovery economics depend on six variables: aircraft type, engine condition and remaining green time, market demand for the airframe family, the speed of the teardown, the quality of records, and the realized price for materials. Reliable benchmarks are hard to publish (each aircraft is unique), but practitioners typically describe the spread as follows.

Sustainability angle: Every kilogram of certified USM placed back in service displaces a kilogram of new OEM production. The mass-balance reporting that comes out of AFRA-accredited disassembly is one of the cleanest scope-3 emissions reduction stories an asset owner can publish, and it is increasingly being asked for by lenders and insurers.

For an end-of-life narrowbody with serviceable engines, engine USM frequently accounts for 50-70% of the total recovery value, with airframe LRUs (avionics, gear, APU) making up another 20-30%, and final scrap recovery making up the balance. For older widebodies, the engine share can be even higher because the spare-engine market continues to demand specific variants long after the aircraft type has exited the front-line fleet.

Aircraft auction online platforms and aircraft disposal company partnerships are now the dominant routes for monetizing both whole aircraft and harvested parts. The decision is rarely binary; most modern playbooks combine a teardown agreement with a parts-sale program and a residual auction event for slower-moving inventory. Listings for salvage aircraft for sale and curated catalogs of aviation surplus parts have also become standard search categories that aftermarket buyers actively monitor, so investment recovery teams should make sure their inventory is visible on the major aviation aftermarket platforms in both formats.

ESG, Scope-3, and the Investor Story

Aircraft retirement is an ESG event whether or not the asset owner chooses to report it. Done well, it lowers scope-3 emissions, contributes to a credible circular economy in investment recovery story, and produces clean evidence for sustainability disclosures. Done poorly, it creates regulatory exposure (especially for hazardous materials) and reputational risk if photographs of poorly managed boneyards surface.

The signals investors and lenders now look for include AFRA accreditation across the disposition chain, third-party mass-balance audits, documented airworthiness traceability, and avoided-emissions calculations expressed in tonnes of CO2-equivalent. This is the same standard that sustainable asset recovery programs in other heavy-industry verticals are converging toward.

Common Pitfalls and How to Avoid Them

Even well-run organizations stumble on the same three issues when they enter aircraft retirement for the first time.

The first is distressed timing. Asset owners who park an aircraft without a clear teardown plan end up making rushed decisions when storage fees mount. Build the retirement schedule before parking, not after. Macro-economics also matter: in a year when buyers wait two extra quarters for industry demand to recover, recovery prices can move 8-10% even on the same aircraft. Tariff and trade policy shifts add another layer of complexity that asset managers need to model.

The second is weak records. Missing or incomplete maintenance records are the single biggest cause of lost USM value. Begin records compilation 12-24 months before retirement, not at teardown.

The third is single-channel marketing. Relying on one broker, one auction, or one direct buyer leaves money on the table. A modern playbook runs USM through certified distribution, online marketplaces, and an aircraft auction online channel in parallel, with pricing discipline by part category.

Frequently Asked Questions

Sources and References

- Fortune Business Insights, Commercial Aircraft Disassembly, Dismantling & Recycling Market, 2026 – market size and CAGR projections through 2034. Source.

- SNS Insider, Used Serviceable Material (USM) Market Size to Reach USD 10.86 Billion by 2033, 2026 – USM market sizing and engine-segment share. Source.

- Aircraft Fleet Recycling Association (AFRA), Best Management Practice Guide v2.0 – accreditation requirements and disassembly standards. Source.

- Boeing Services, Aircraft Recycling Program – OEM disposition framework and material recovery references. Source.

- Airbus, Global Services Forecast 2024-2043 – $52B USM value forecast over twenty years (cited in industry reporting).

- GlobeNewswire, Aircraft Recycling Industry Report 2026-2031 – $5.06B 2025 market sizing and growth drivers. Source.

- ICAO Environmental Report 2016, AFRA – Leading the Way in Safe and Sustainable Aircraft Recycling – background on AFRA and BMP. Source.

- AerSale, USM and You: How Airlines Can Benefit From Used Serviceable Material – USM pricing and supply chain context. Source.

Disclaimer: This article is published by the Investment Recovery Association (IRA) for educational and informational purposes only. It does not constitute legal, financial, or professional advice. Market data, statistics, and projections cited are sourced from third-party reports and are subject to change. Readers should consult qualified professionals before making business decisions based on the information presented. The IRA makes no warranties regarding the accuracy or completeness of third-party data referenced herein.